2019 Q3: An Antidote to Noise Distraction

Tuesday, October 01, 2019

Investing in stocks that pay dividends now and grow their dividends over time will help you remember that your goals are longer term than next quarter or next year.

Investing in stocks that pay dividends now and grow their dividends over time will help you remember that your goals are longer term than next quarter or next year.

Considering the relatively benign performance of the equity markets this past quarter, the degree to which background noise is bothering both bulls and bears is somewhat surprising. There is always noise—items to worry over, visions of downsides and upsides that may be in the future but don't exist in the present. Always the noise of experts and strategists who claim to know just precisely what to do to make great investment gains in the next quarter or two. Always the noise of scandal, of earnings beats and shortfalls, of fees and flows, new products, new competitors, changes at the top, trends and demographic epochs—the constant noise against which decisions have to be made.

Today the issues are a big earful: Brexit, impeachment, US/China trade wars, mini interest rates, recession predictions, negative rates in Europe dragging everyone down, the Fed and whether it is ahead or behind the curve (and the rate curve itself!), bombing in the world's largest oil fields, climate change, the upcoming US election, the schism between the manufacturing and service economies, creepy data stealing our souls, record employment but little change in incomes, income inequality. Oh, and there's the matter of record-high valuations induced by those record-low interest rates.

How can an investor make decisions when faced with such an array of imponderables and their doubly imponderable consequences, amplified to screeching volume by the incessant debate about what matters and what the future will look like, buffeted about as it might be by the outcome of all these unknowns? In years past, many flummoxed investors fled to bonds.

The Quiet, Slow Decline of Bond Yields

John Authers of Bloomberg cites a recent Deutsche Bank long-term study led by Jim Reid concluding that the decades ahead "are unlikely to be good for bondholders."1 Reid's group notes that, at present, "the European market is priced for negative rates for another seven years, which means that investors expect the longest period of financial repression in more than two centuries, other than the aftermath of World War II." Considering the fact that real yields (bond yield minus inflation) on government debt are now negative, by way of corollary the authors conclude that "we are at the beginning of the longest period of sustained negative real yields in history." Or so "speak" the bond market and futures traders.

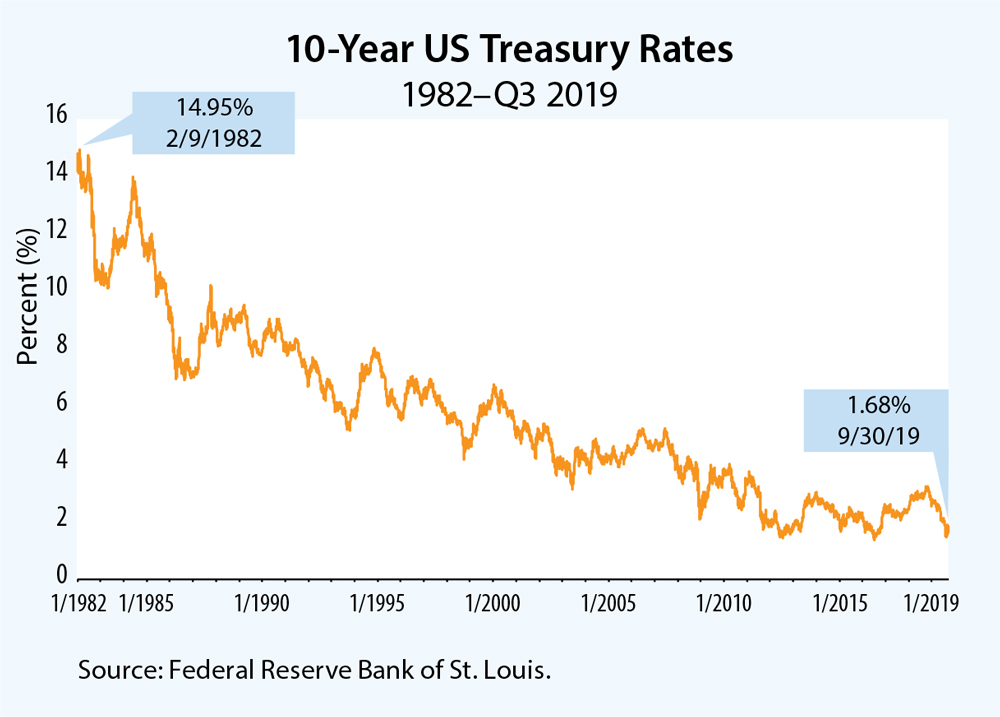

But that sets the stage for governments to borrow at low (or even negative) rates and spend, spend, spend to try and stimulate growth in the economy (despite the severe demographic headwinds of an aging population in the world's economic powers, from Europe to the US to China and Japan). Here is where it gets vicious, because you don't have to be an economist to know that when governments crank up the presses and programs, inflation is not likely to lay dormant, which means interest rates are likely to rise (no, not this quarter!) and bonds are then likely to fall. How much? Rates peaked in 1982 and have declined since then, going on almost 40 years. Is there a law somewhere that says such a trend can't be reversed, perhaps even in an equal and opposite way?

What Fixed Income and Cement Have in Common

After nearly four decades of bond plenty for investors, the dark side of the moon has been obscured. But it is still there. When rates rise, bond prices must fall. It's just math. The impact on stocks or metals or commodities or real estate isn't fixed, it's variable. Fixed income, though, correlates directly with prevailing interest rates. It's fixed at issuance, always—like cement.

So long-term investors can assume that bonds will induce losses in the years to come. Maybe not this year, maybe not next year, but eventually politically motivated stimulus will result in inflation—or inflation may just come on its own, as it always has. At that change point the pain of negative real rates will drive the yields of bonds higher and prices lower. Because yields are set when bonds are issued, any given bond can't compete with the reduction in purchasing power that bonds will "provide."

Inflation Is Not a Given

We've avoided the knee-jerk reaction of "cycle" hobbyists for years, remaining sanguine about inflation, though the common reaction to record-low unemployment was that inflation was inevitable. Milton Friedman's holy observation that inflation is "always and everywhere a monetary phenomenon," a tenet of faith in the finance world, is apparently, after more than a decade of pump-priming, totally dead. Yes, he and others didn't take into account the generalized economic drag of aging populations in the world's developed countries, continued horizontalization of production in low-cost countries, and the fact that bond rates are a far better predictor or "analyst" of inflation's present and future than the largest shouting army of sell-side strategists. In a sense, bond rates anticipated and discounted the current fad for claiming "recession" many quarters ago. Rates reflected modest and declining demand for money as manifest in the continually dwindling velocity of money that we've pointed to many times. Still, there is always the possibility of renewed inflation—the reason might not be predictable now—so that chance needs to be addressed in any strategy.

A Counter to Noise Fatigue

In a sense, given the noise all around, the noise we've pointed to above, there's only one question for investors: Are you a long-term investor or not?

The answer doesn't necessarily depend on whether you proceed as a buy-and-hold investor in individual securities or one who moves around, but on whether or not you see yourself as investing over a period of many years. If so, do you want to invest where there is a high probability of inflation-adjusted loss, or do you want to invest where you at least have the potential to grow despite whatever volatility may lie ahead?

As income-oriented equity investors, we want to know about our future income, not necessarily about today's low rates, since today will soon enough become yesterday.

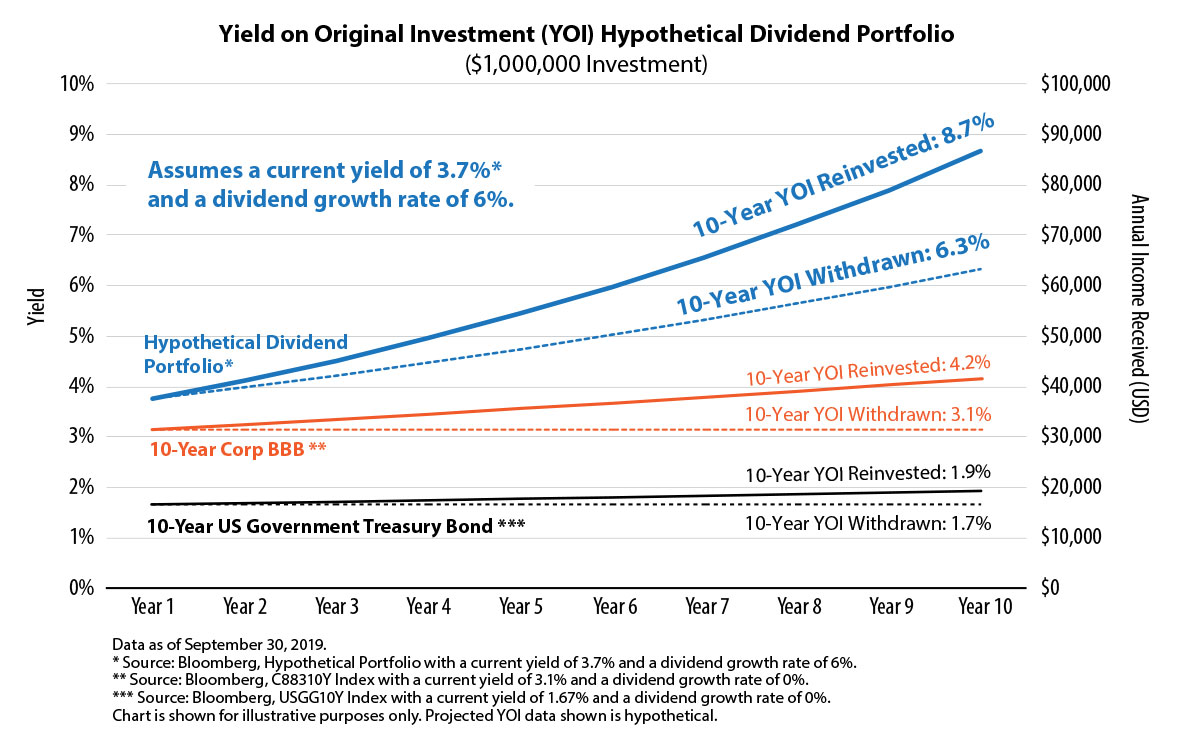

We want to know what our future yield on original investment (YOI) will be, and we want it to be higher. The markets may rise and fall—one year the P/E may be 20 and another the P/E may be 10. But income from carefully selected dividend stocks will have far lower volatility than stock prices—in fact, by definition income is always positive—and ideally the income is what you should spend. Sure you can spend from principal, but at any given time, what will the principal actually be? Too tough to call, we think. Over time, rising income can help induce rising principal values (the inverse of rising interest rates, which cause bonds to fall). How much, how fast, and how soon are functions of both current valuations and unknowable future developments in prosperity. But if we are making decisions today, given that the future is never certain, income—that one investment feature that is always positive—is a good place to start.

A Future of Positive (and Growing) Income

Based on our Yield on Original Investment Calculator, we envision a future starting from current conditions (see chart below).

Interestingly, in today's noisy world investors are told they can get 1.7% for a "safe" US 10-year or 3.1% for a BBB-rated 10-year (that's 2 half-notches away from noninvestment grade), despite inflation running ~2%—and they still go for it! But we're at an unusual moment in history where it is easy to get a higher starting yield from even BBB-rated equities than from bonds, and there is the possibility that the dividend from the equities can grow. Assuming a modest 6% growth rate going forward and reinvestment of income, an equity that yields 3.7% can reach a yield on investment of nearly 9% within a decade. In a well-managed portfolio the yield on original investment can continue to grow similarly.

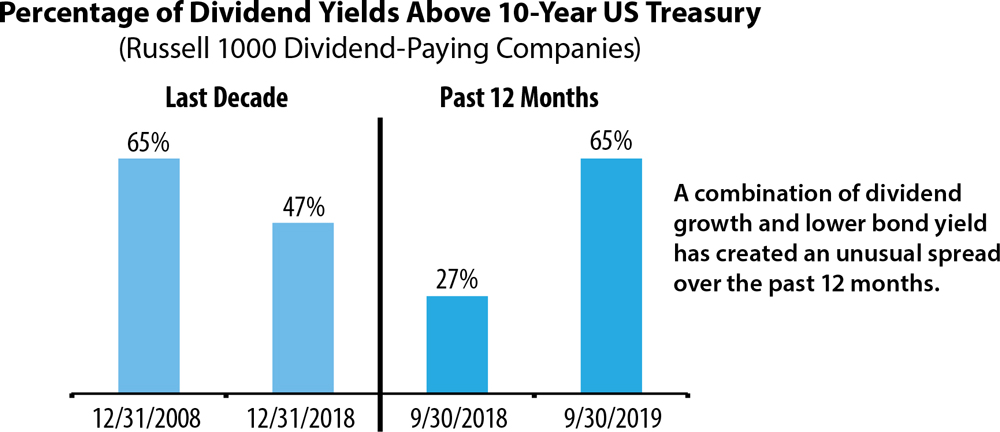

Even without considering the future growth of income, we're at a rare moment in which more than 60% of dividend-paying stocks offer a higher yield than 10-year Treasuries.

Income Investing—The Time Is Ripe

More than 30 years ago, when we first wrote about dividend investing compared to fixed income, we simply assumed that the starting yield for a dividend portfolio would be 1–2 percentage points lower than bond yields (and this was at a time of bond yields much higher than today). We also assumed that it would take 4–5 years of dividend growth before one's yield on original investment would equal the bond yield—then surpass it over time as dividends continued to grow. But today the average yield is 1 percentage point higher than bonds, not lower (and it is not too hard to construct a portfolio that is 2 percentage points higher). So in the race for income over time, it is something like starting a 5-mile race with a 4-mile lead!

This is a ripe moment. The last time stock yields were clearly much higher than bond yields was 2008 and its aftermath, when stock current yields were temporarily elevated because stocks declined, and bond yields were suppressed because the Fed rushed to save the world with lower rates. All the while, everything from the economy to the financial markets crashed sharply.

Last quarter we asked "Is the End Really Near?" It wasn't, in our view, and it isn't now. There is volatility, yes, and there is noise, and there are witch doctors shaking rattles across the landscape pointing fingers and showing charts about recession. But if you're seeking long-term results and hoping to avoid running to one side of the ship and then the other, try focusing on income production rather than getting scared by the noise. This can help neutralize the inevitable fears and uncertainties that arise. Investing in stocks that pay dividends now and grow their dividends over time will help you remember that your goals are longer term than next quarter or next year. In a world of noise, an income focus can help buy you peace and quiet.

1 Bloomberg, Bonds are on the Road to Nowhere, aka the 70s.

BENCHMARK DEFINITIONS

C88310Y Index: BFV USD Composite (BBB) 10 Year — A Bloomberg composite of yields derived from BVAL-priced bonds.

USGG10YR Index — US Generic Government 10-Year Yield—Yields are yield to maturity and pre-tax. The rates are comprised of Generic United States on-the-run government bill/note/bond indices.

Lowell G. Miller founded Miller/Howard Investments in 1984. Lowell has served as President and Secretary of Miller/Howard's Board of Directors, as well as President (Principal Executive Officer and Trustee) of Miller/Howard High Income Equity Fund, and Chairman of the Board of Trustees of Miller/Howard Funds Trust, since the funds’ inceptions in 2014 and 2015, respectively. He began his studies of the securities markets as an undergraduate and has continuously pursued the notion of disciplined investment strategies since 1976. He is the author of three acclaimed books on investing, including The Single Best Investment: Creating Wealth with Dividend Growth (Print Project, 2nd Edition, 2006). He has also written on financial topics for The New York Times Magazine, and has been a featured guest on Louis Rukeyser's Wall $treet Week and Bloomberg TV. Lowell is frequently quoted in financial media such as The Wall Street Journal, Dow Jones Newswires, Bloomberg, Fortune, and Barron's. He holds a BA in Philosophy from Sarah Lawrence College and a Juris Doctor degree from New York University School of Law.