A Case Study on Compounding: Old Republic’s Dividend Story

Wednesday, June 14, 2023

At Miller/Howard, we are big believers in the benefits of high dividend paying stocks.

Recently, we were offered yet another example of the power of compounding dividends. We added Old Republic International Corp. (ORI) stock to our Income-Equity Strategies in January 2018 at around $20 per share. Old Republic, a specialty insurance company, was exiting the mortgage insurance business and had put it into “runoff.” The specialty insurance business was doing well, and as the mortgage insurance business wound down and released excess capital, ORI committed to pay that excess capital out to shareholders as special dividends—this is in addition to its regular, quarterly payouts from the ongoing businesses. Over the years, ORI’s businesses did well, and it continued to pay and raise its regular dividend. As capital was released from the “runoff” business, it also paid four special dividends.

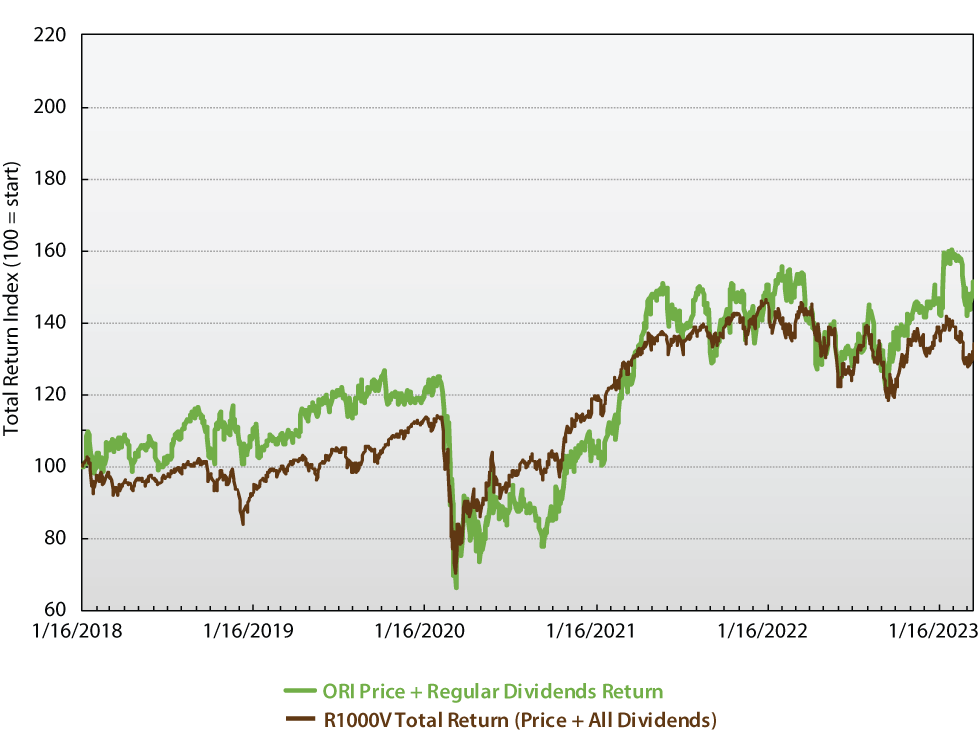

Looking only at the return from the price appreciation, Old Republic did a little better than the Russell 1000 Value Index (R1000V). From when we purchased it until the end of the first quarter of 2023, ORI’s annualized price-only return was +5.8%, while R1000V’s annualized price only return was +4.8%. Good outperformance, but not too remarkable.

and the Russell 1000 Value Index (R1000V)

| Annualized Returns from January 16, 2018 to March 31, 2023 | |||

|---|---|---|---|

| ORI | R1000V | Difference | |

| Price Only | +5.8% | +4.8% | +102bbs |

* As of March 31, 2023. Sources: Morningstar; ORI website; Miller/Howard Research & Analysis. Note: The start date represents the addition of ORI to the Miller/Howard Income-Equity Strategies.

Dividends Make A Difference

As we described, Old Republic pays a substantial regular dividend in addition to recent special dividends. When looking at the returns of both ORI and R1000V, including both price and regular dividends (but not the special dividends), ORI has clearly outperformed R1000V, +11.8% to +8.2%, respectively, over this period. A higher dividend yield, along with the power of compounding from reinvesting that higher dividend resulted in significant outperformance and added to wealth creation for shareholders.

and the Russell 1000 Value Index (R1000V)

| Annualized Returns from January 16, 2018 to March 31, 2023 | |||

|---|---|---|---|

| ORI | R1000V | Difference | |

| Price Only | +5.8% | +4.8% | +102bbs |

| Price + Regular Dividend | +11.8% | +8.2% | +354bbs |

* As of March 31, 2023. Sources: Morningstar; ORI website; Miller/Howard Research & Analysis. Note: The start date represents the addition of ORI to the Miller/Howard Income-Equity Strategies.

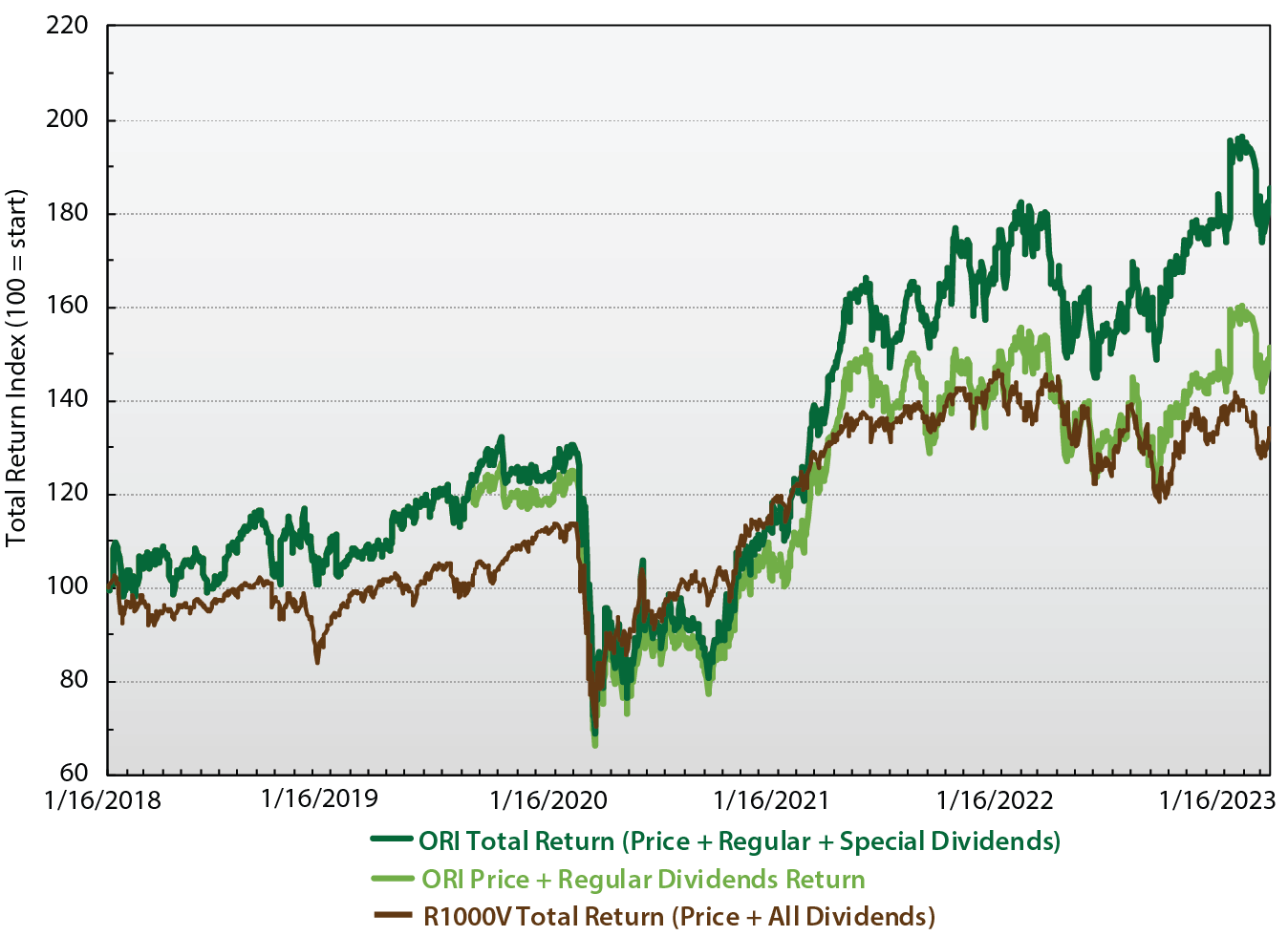

However, there’s more: Remember when we mentioned that in addition to regular quarterly dividends, ORI paid special dividends as a way to return excess capital to shareholders? When those special dividends are included, ORI’s total return is even more impressive. Despite a price-only return just a little more than the benchmark, the higher quarterly dividend along with the four special dividends over this period resulted in ORI’s annualized total return (price appreciation, plus reinvested regular dividends, plus reinvested special dividends) of +18.1%, which was +982 basis points higher, or over double, the annualized total return of R1000V.

and the Russell 1000 Value Index (R1000V)

| Annualized Returns from January 16, 2018 to March 31, 2023 | |||

|---|---|---|---|

| ORI | R1000V | Difference | |

| Price Only | +5.8% | +4.8% | +102bbs |

| Price + Regular Dividend | +11.8% | +8.2% | +354bbs |

| Price + Regular + Special Dividend | +18.1% | +8.2% | +982bbs |

* As of March 31, 2023. Sources: Morningstar; ORI website; Miller/Howard Research & Analysis. Note: The start date represents the addition of ORI to the Miller/Howard Income-Equity Strategies.

Clearly, compounding income—from all of the regular dividends and specials paid by ORI—had a material impact on its shareholders’ return. Of course, ORI’s dividend compounding story is not unique; compounding’s magic happens to any stock with steady income, but the larger the income stream, the faster the compounding, and the more wealth created.

Perhaps the best part of compounding is that the power of compounding doesn’t depend on being able to forecast earnings, or economic conditions, or interest rates, or politics, it just takes income, time, and mathematics.

John (Jack) E. Leslie III, CFA, focuses on diversified, dividend-paying stocks. He is a member of Miller/Howard's Board of Directors. Prior to joining Miller/Howard in 2004, Jack was a portfolio manager at Value Line Asset Management, M&T Capital Advisors Group (a division of M&T Bank Corp.), and Dewey Square Investors Corp. (now part of Old Mutual Asset Management). Jack earned his BS in Finance from Suffolk University and an MBA from Babson College.