Are the Stars Aligning for Energy?

Thursday, March 14, 2019

At Miller/Howard Investments, we believe the energy market is at a critical inflection point. There are key macro supply and demand developments that should benefit companies within and around the North American energy sector.

Supply Drivers

The US continues to gain global energy market share, aided by the shale revolution. Over the next decade, as the US moves to become a major net exporter of petroleum and refined products, we expect a tailwind across the broader value chain—from the producers in the field, to the equipment and service providers, the pipelines and processors, and those owning contracts to ship around the world.

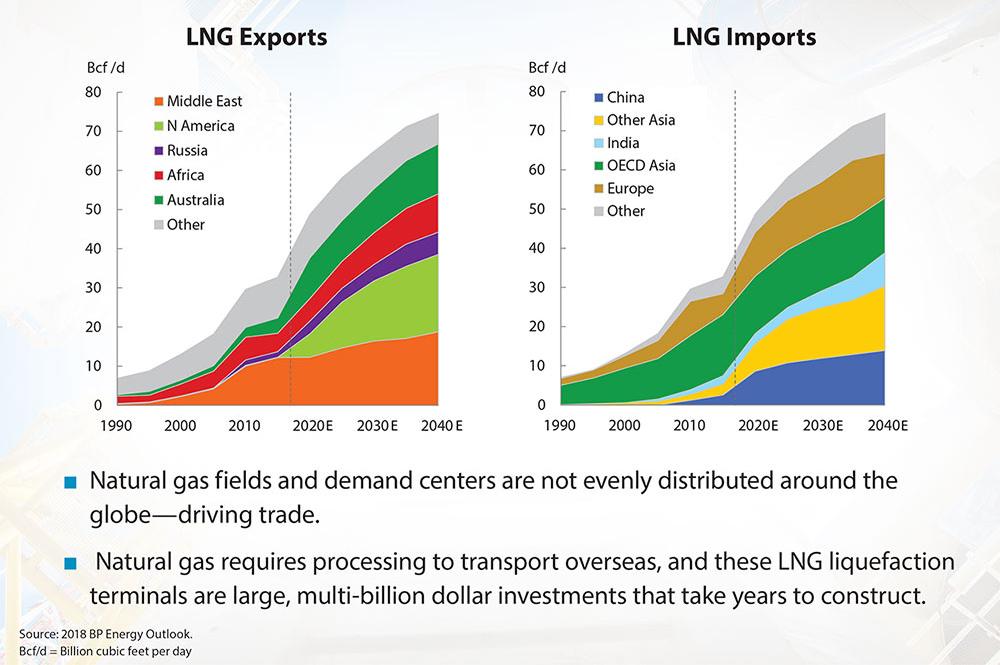

The US is also projected to more than double its liquefied natural gas (LNG) exports aided by six new LNG export facilities entering service this year. Keep in mind these facilities are multi-billion-dollar projects that have taken several years to build. And many of these export facilities already have signed, multi-decade, take-or-pay contracts. A seventh facility is under construction that will take five years and cost over $10 billion to construct.

Success in the Permian Basin has been somewhat muted by lack of energy infrastructure. Pending buildout of this needed infrastructure is projected to double oil production in the Permian over the next 5 years.

But aren’t we opening ourselves up for a possible replay of 2015 when the deluge of US shale oil supply doomed the markets? That’s not the case, in our view, due to international supply constraints that are creating a “Tale of Two Cities.”

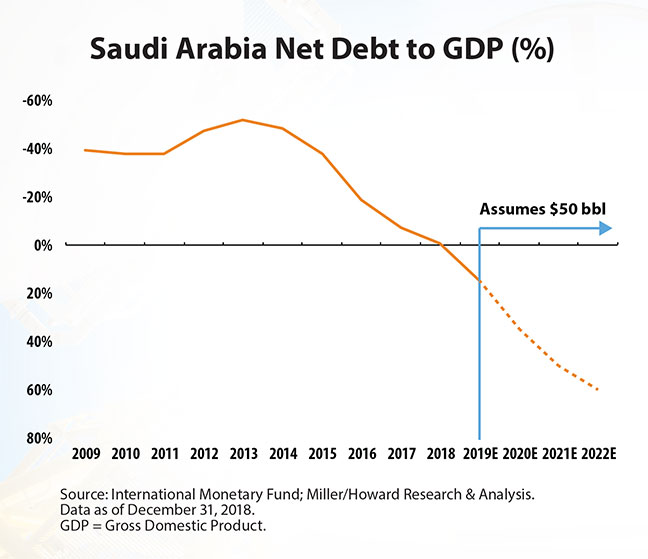

The other “city” is Saudi Arabia, which currently produces 11% of the world’s oil and is, by far, the largest exporter. In a nutshell, Saudi Arabia is like an oil company with a decent balance sheet that’s bleeding cash. Though producing oil is cheap in the Saudi desert, maintaining peace and stability in a kingdom of 33 million, plagued by poverty, costs hundreds of billions of dollars.

Saudi Arabia is simply not fiscally sustainable below $80/bbl Brent oil. They no longer have the rainy-day funds to fight another price war with US shale.

Instead, Saudi Arabia has, in our view, moved to a strategy that will continuously cede small amounts of market share to support price, with the belief that shale will gain share through the late 2020s, when they hope to participate in growth again. The math is simple—if OPEC can double the price that they receive for oil merely by cutting their supply by 5-10%, they will generate more revenue with less production. We believe this is exactly what they will do.

Also impacting global supply are Iran and Venezuela, traditionally major oil exporters. Iran is facing severe US sanctions while Venezuela is fighting through unrest and potential civil war. We expect reduced exports from these two oil exporters.

Demand Drivers

What is the US going to do with all this increased supply, and how might this benefit energy investments? The answer lies in the corresponding increase in demand from Asian countries — China, in particular.

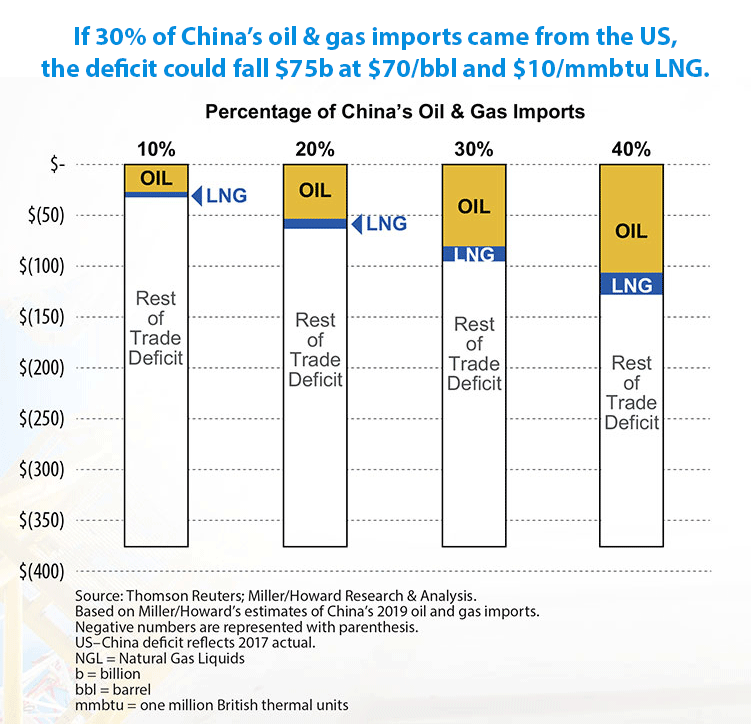

Today, the American trade deficit with China runs about $400 billion per annum. Each of the bars in the chart below shows how much of a dent the US could potentially make in our trade deficit by meeting a certain percentage of China’s energy import needs, which are growing rapidly. In the case of LNG, China’s demand is currently growing at an astounding 40% per year.**

However, as we all know, the US is locked in a trade dispute with China. A key stated objective of the Trump administration is to reduce the trade deficit, and energy is one of the few products we produce on a cost-competitive basis.

We believe an accord will eventually be reached with China, with American energy exports as a centerpiece of any trade agreement.

China is even more reliant today on the unstable Middle East and Russia than we were 10 years ago—before shale. As a result, it appears that China would very likely welcome the opportunity to diversify their exposure. And American energy companies will be willing trade partners.

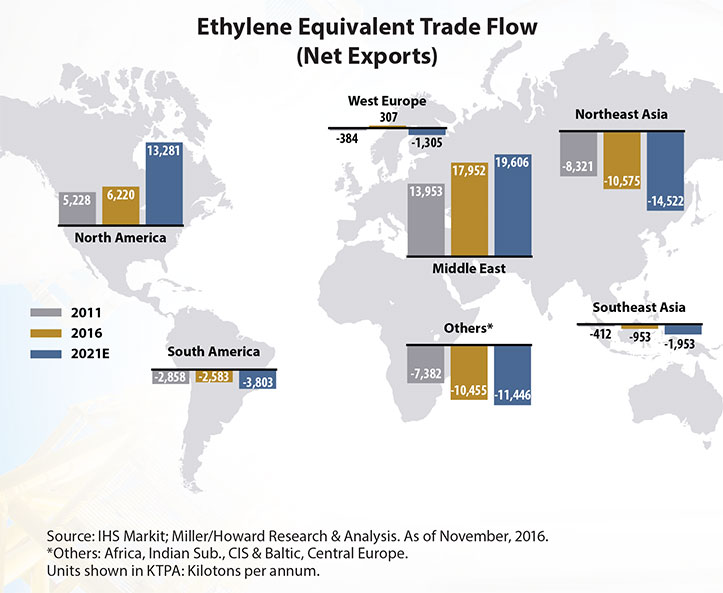

Another major growth driver, in our opinion, for American natural gas and natural gas liquids (NGLs), is plastics. Yes...plastics!

Our plastics exports are set to ramp dramatically over the next 24 months, as the US begins to ship more of our cost-advantaged product to Asia and Africa — countries that are currently buying their feedstock from Russia, the Middle East, and Australia. This will boost demand across the entire energy value chain. Energy comprises 90% of the cost of making plastics, and the US is a global low-cost supplier.

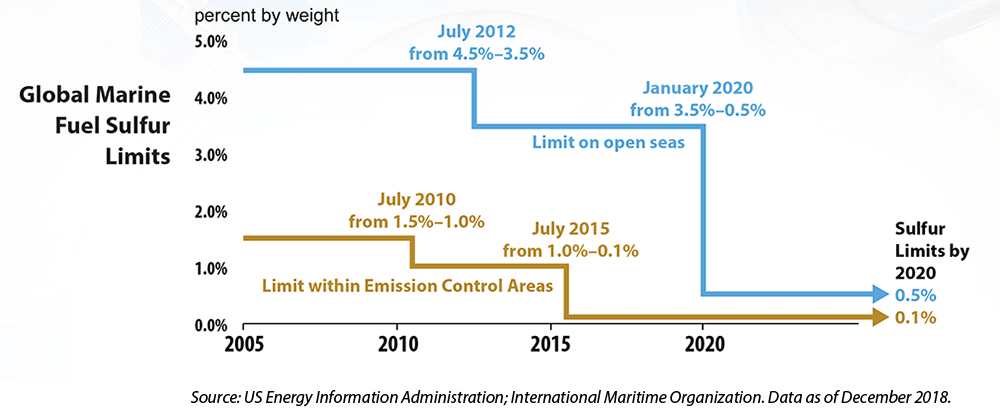

The final growth driver is a little-known agreement—the International Maritime Organization regulations, or IMO 2020—designed to reduce the sulfur content of fuel used by the shipping industry.

We believe this standard will substantially increase global demand for crude oil in the latter half of 2019 and into 2020, and that it will support higher oil prices.

Why does higher-quality fuel mean increased oil demand? The details are technical, but based on existing refinery infrastructure, in order to create enough high-quality fuel, refiners must process more crude oil. How much more? We estimate that it’s about 500,000 barrels per day. This is in comparison to “normal” oil demand growth of 1.5 million barrels per day. So, we believe IMO 2020 will boost oil demand growth by about 30% over the next 18 months.

To Wrap Up

We believe:

- It is an ideal time to capture what we see as the new global energy landscape driven by the US shale revolution.

- America will reap the benefits of global emerging-market-driven energy demand.

- Natural gas will play a growing role in society going forward, particularly in the emerging area of LNG exports.

- It is important to take advantage of these developments along the entire US energy value chain, as the shale revolution is contributing to growth opportunities for producers, processors, pipelines, contractors, and the export terminal owners.

** China National Bureau of Statistics.

Michael Roomberg, CFA, focuses on diversified, dividend-paying stocks as well as the energy sector. Before joining Miller/Howard, Michael served as head of water/infrastructure equity research at Ladenburg Thalmann & Co. in New York City. Prior to that he served on Jefferies’ Industrials equity research team. Michael began his career as a research associate at Boenning & Scattergood Inc., a financial services firm in greater Philadelphia, where he specialized in energy exploration & production, and water utilities and industrials. Michael earned his BA in International Relations, Economics, and Finance from University of Wisconsin-Madison. He holds an MBA from the McDonough School of Business, Georgetown University.