Are your Dividends at Risk?

Monday, June 22, 2020

Active Dividends

Active management may have benefits over passive management during times of uncertainty—especially for investors who prioritize dividend stability.

- Passive investments often provide exposure to a specific area of the market—such as stocks with high dividend yield or a history of dividend growth.

- Periods of stress can highlight the risks inherent in the backward-looking nature of index construction. Many indexes rebalance only once or twice a year, leading to stale constituents if revenues, stock prices, or dividend policies change.

- Each market crisis is unique in both what causes the crisis, and, more importantly, investors’ outlook coming out of the crisis. Stocks that were rewarded before a crisis hits may not fare so well in the rebound.

- Active stock selection provides flexibility to invest in quickly changing markets, while still maintaining your overall investment objectives.

COVID-19 has ushered in an era of uncertainty for investors, and for now, we can’t be sure if a cure or a second wave is coming around the corner.

We believe dividend investors may be at an advantage in this uncertain environment.

Dividend investors understand that future stock prices are unpredictable, as stock prices can be driven as much by investor sentiment as by fundamentals. They understand that stock prices, historically, are more than six times more volatile than their underlying dividend cash flows (based on the S&P 500 Index from 1957-2019), as sentiment drives short-term prices while fundamentals drive long-term value.

- In the 62 years since the inception of the S&P 500 Index (1957-2019), price return has been negative 18 times with an average negative return of -11.5%.

- Dividend growth, on the other hand, has only been negative 6 times, with 2009 the only time it decreased by more than -3.5%.

Investors typically do not like to see unrealized losses on their statements. However, dividend investors tend to focus on the income line item on their statement instead. As long as the income continues, they can endure the market volatility and wait for stock prices to recover as the pandemic—or other market turbulence—wanes. In addition, during economic downturns, dividend investors may have an opportunity to use the income they receive to purchase additional shares at a discounted price. As we have written before, this can be especially beneficial when combined with the power of compounding dividends.

Periods of market stress often highlight the advantages of active management. This is especially true when managing for dividend stability.

The metrics that drive dividend stability and prospects for growth are more fundamental than sentimental. Active managers may ask:

- What is the company’s dividend obligation—and how committed is management to paying that dividend going forward?

- What is the dividend coverage ratio (i.e., how much is the company making versus the dividend payments)?

- Is the company’s leverage appropriate for the business and the industry?

- What other cash obligations does the company have in the near-term and medium-term?

- What are the company’s revenue and profit projections, and are they realistic? Passive strategies are unable to ask these questions.

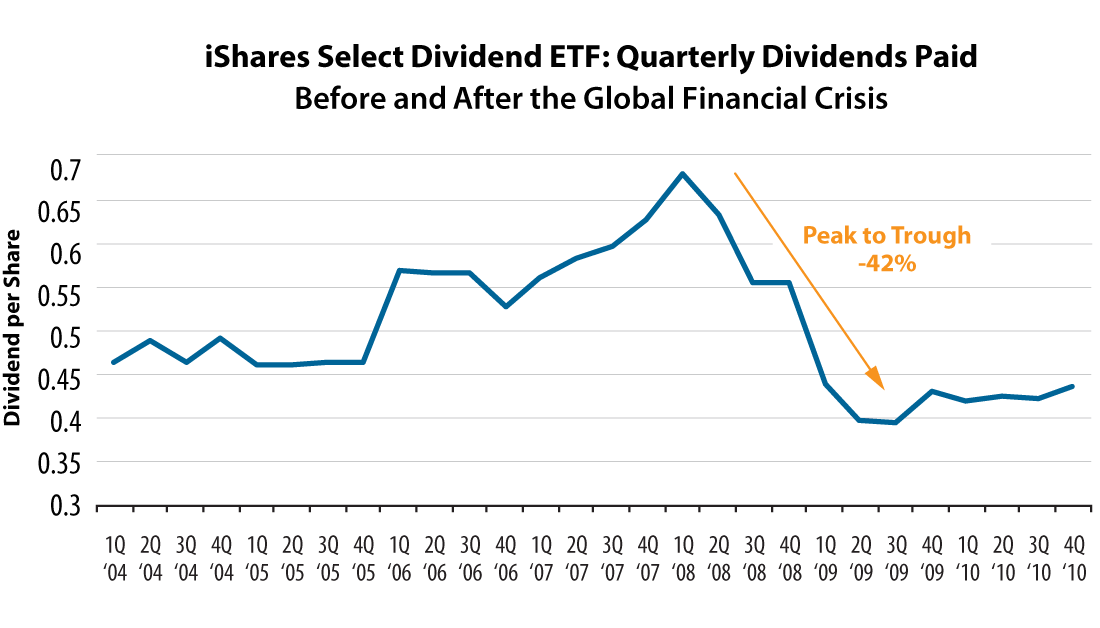

Following the Global Financial Crisis, 2009 was a challenging year for dividends. For dividend investors (in particular, investors that rely on dividend income to meet their spending needs), the trauma of 2009 is a fresh memory. S&P 500 dividends declined by -21% in 2009, the largest decline by far throughout the history of the S&P 500.

Such a steep decline in dividend payments was especially jarring to investors that had quietly collected dividend payments and considered them a “safe” part of their portfolio. Investors in passive dividend ETFs quickly learned the shortcomings of an investment strategy that is determined by historical attributes (for example, a history of consistent dividend payments) versus prospects for and commitment to future dividend payments.

Source: Bloomberg; Miller/Howard Research & Analysis

One example, the iShares Select Dividend ETF (Ticker: DVY), which tracks the Dow Jones US Select Dividend Index, saw its dividend decrease by -37% for June 2009 versus June 2008. Making matters worse, the underlying index had its annual rebalance in March 2008, just as dividend suspensions were starting to surge.

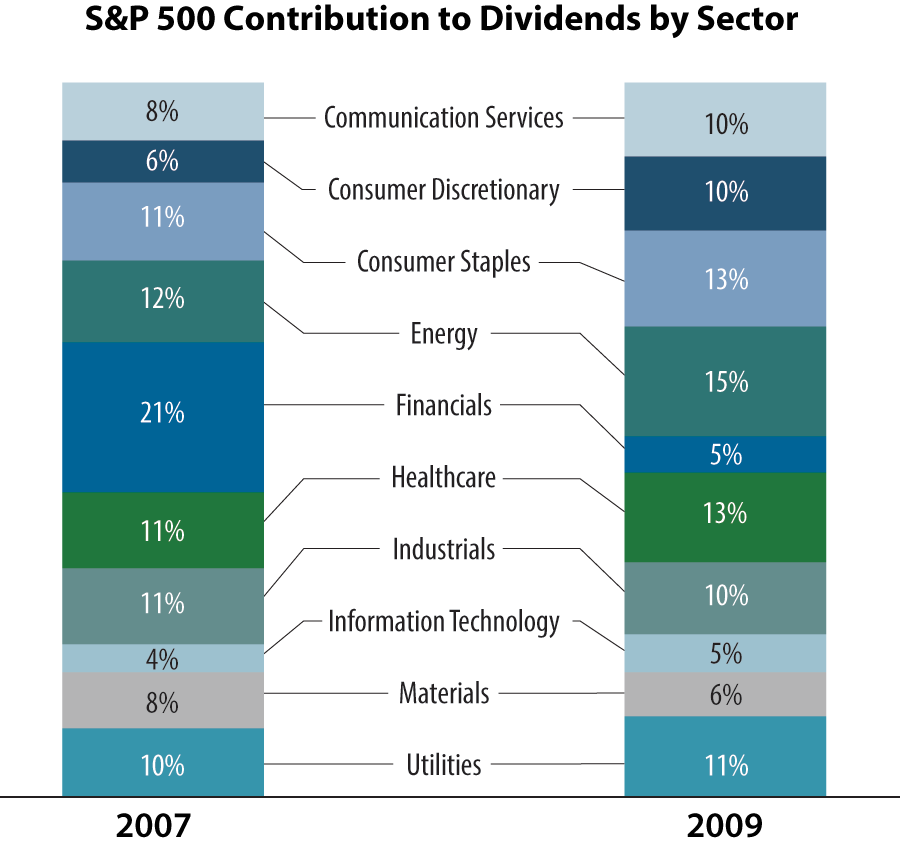

Financials were at the center of the Global Financial Crisis. Compounding the pain for dividend investors, financials also made up a significant portion of dividends per share for the S&P 500 in 2008. The share of S&P 500 dividends for the financial sector shrank from 21% in 2007 to 5% in 2009. One condition of participating in the US Treasury’s Troubled Asset Relief Program (TARP) was that banks had to suspend their dividend payments. Not surprisingly, DVY was heavily exposed to financials at the time.

Active managers were able to follow the terms of TARP as it evolved and trade out of financials that were in danger of eliminating their dividends—but many ETFs, with their backward-looking rules, had to continue to hold these stocks. Too, the crisis eventually passed. Many dividend cutters found firmer financial footing and began to increase their payouts again, but certain ETFs couldn’t participate—they required a history of dividend increases that had been broken and reset.

Source: Bloomberg; S&P; and Miller/Howard Research & Analysis

Today’s corollary to TARP might be the CARES Act (Coronavirus Aid, Relief, and Economic Security Act) that also limits the payment of dividends by any company that borrows money from the US government. In many cases, this restriction lasts for one year after the loan is paid back. But unlike TARP, that focused on the financials sector, the CARES Act could restrict dividends for companies across all sectors—though some sectors, such as energy and consumer discretionary, will likely be more impacted than others.

Ultimately, the impacts of COVID-19 are widespread, and simply selecting the ‘right’ sectors or industries may not be enough to protect dividend income.

Past dividends do not guarantee future results.

In our view, investors should, instead, invest in high quality companies with the financial strength to make it through the trough. Bottom-up fundamental research can provide insight into which companies may be over-levered and which firms have strong balance sheets to ride out a period of economic instability. Active management can help to identify the prudent companies that planned for an economic downturn.

Actively managing for dividend stability means finding companies that are best able to continue to pay their dividends, and will be ready for dividend growth when the current storm passes.

The best feature of passive approaches—broad exposure to an investment objective like dividend income—may become a liability during times of stress, when investors want to avoid weaker companies. This has become more of a challenge over the last few years with the 10x growth in the number of passively-managed dividend and low-volatility ETFs.

Recessions and periods of market stress are triggered by a broad range of events. But the factors and company fundamentals that signal a stock’s dividend stability remain consistent during the full market cycle. Throughout our history, we have focused on those signals: high dividend yield, prospects for dividend growth, financial strength, and earnings stability.

Sources: S&P, Robert Shiller (http://www.econ.yale.edu/~shiller/data.htm), and Miller/Howard Research & Analysis

John (Jack) E. Leslie III, CFA, focuses on diversified, dividend-paying stocks. He is a member of Miller/Howard's Board of Directors. Prior to joining Miller/Howard in 2004, Jack was a portfolio manager at Value Line Asset Management, M&T Capital Advisors Group (a division of M&T Bank Corp.), and Dewey Square Investors Corp. (now part of Old Mutual Asset Management). Jack earned his BS in Finance from Suffolk University and an MBA from Babson College.