Fixed Income vs. Unfixed Income

Tuesday, January 11, 2022

When most investors think of retirement income, or just investment income in general, they frequently think of bonds and not stocks. “Fixed income” investments such as bonds have provided generations of investors with a relatively safe and stable source of income, especially if the bonds were US Treasuries or high-grade corporate bonds. Unfortunately, that income stability is just that—stable. This can become a problem as inflation raises the cost of living while income remains flat, and a “fixed income” becomes an even larger problem as inflation rapidly rises.

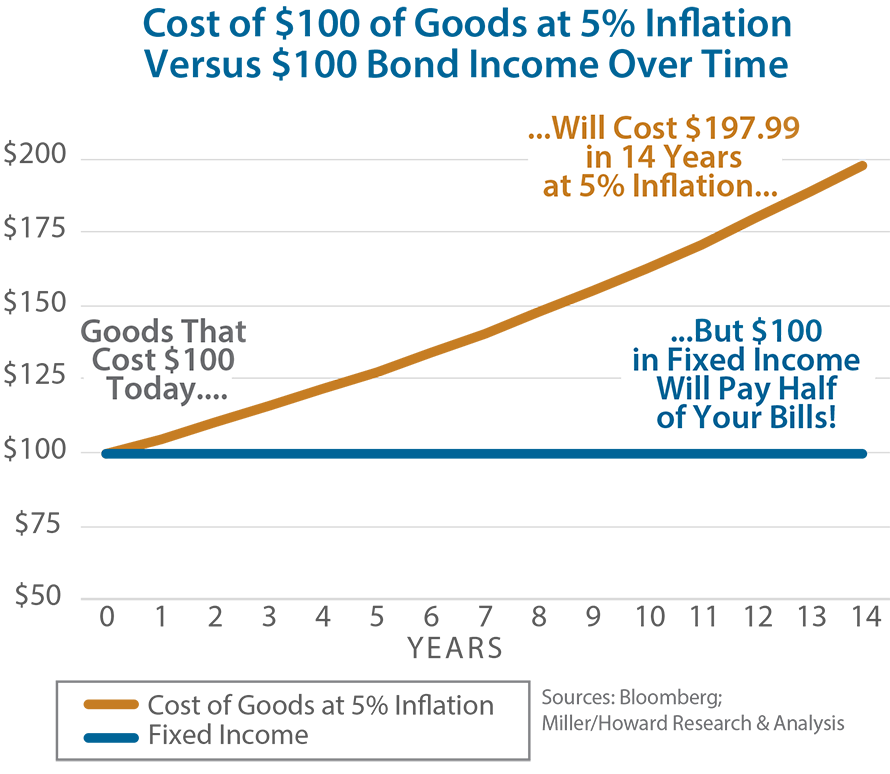

Inflation eats away at your ability to afford your current life style. Even at an annual inflation rate of 5%, prices double in 14 years. This 5% assumption is well under the most recent reading of 6.8% for consumer inflation and 9.6% for raw materials and manufacturing inputs (future inflation?). If current trends persist, prices could double sooner. Put another way, when prices double, it would be like trying to live now on half of your income. What expenses would you need to cut to survive on half of your current income? What pleasures would you need to eliminate from your life?

We view dividend-paying stocks as a potential solution—with a focus on companies that have the potential to raise their dividends consistently over the long term. As prices rise, so too should corporate profits, allowing some companies to increase their dividends in-line with inflation. We call this “unfixed income”. These “unfixed income” investments could allow your income to keep pace with inflation and help you maintain the same standard of living that you enjoy now well into the future.

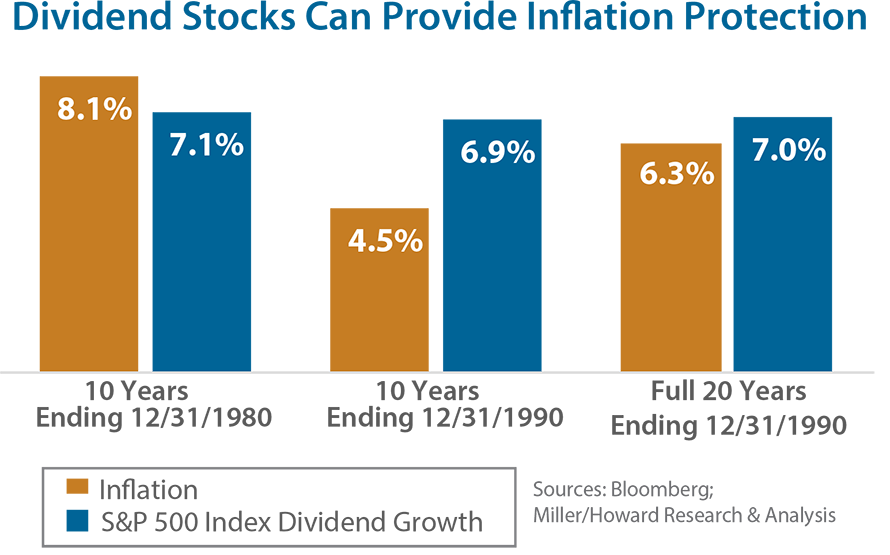

Over time, dividend growth has broadly kept up during periods of high inflation, as can be seen during the 1970s and 1980s, the last time the US experienced a prolonged period of high inflation. (Inflation has been generally muted over the past several decades, so we need to look back in history to find a comparison.) In the ten years ending December 31, 1980, when prices rose at an annualized +8.1%, dividends for the S&P 500 Index grew +7.1% per year. Dividends didn’t quite keep up with the more than doubling of prices during that decade, but they did help to protect purchasing power much better than a bond, where interest payments remained unchanged.

Over the subsequent ten years ending December 31, 1990, price inflation moderated to “only” +4.5% per year, but this time dividend growth outpaced inflation to grow +6.9%. For the combined twenty-year period, inflation was an annualized +6.3% while dividends grew at a comparable +7.0%. Dividends helped investors maintain their inflation adjusted or “real” income levels. Of course, a “fixed income” bond did not provide any income growth over that time.

Given today’s potential for an increase in US inflation and low current interest rates, it may be time for investors to rethink their portfolio strategy and look to increase their investment portfolio’s exposure to dividends for both current income and inflation protection.

John (Jack) E. Leslie III, CFA, focuses on diversified, dividend-paying stocks. He is a member of Miller/Howard's Board of Directors. Prior to joining Miller/Howard in 2004, Jack was a portfolio manager at Value Line Asset Management, M&T Capital Advisors Group (a division of M&T Bank Corp.), and Dewey Square Investors Corp. (now part of Old Mutual Asset Management). Jack earned his BS in Finance from Suffolk University and an MBA from Babson College.