Growth vs. Value

Tuesday, February 19, 2019

At Miller/Howard Investments, we believe successful investing requires both attention to current market fundamentals impacting stock prices as well as consideration of long-term market cycles and trends.

Take, for example, the growth vs. value style cycle. It is of particular interest to investors today as the FAANG-driven bull market seems to have hit a speed bump in October 2018.

Curious market observers will naturally look to previous inflection points in the growth vs. value cycle for clues to stock market behavior moving forward. Not surprisingly, we think we've seen this movie before. After the tech bubble burst in 2000-01, a five-year period where "growth" stocks convincingly outperformed "value" stocks came to a sudden end. Interestingly, the disparity between growth stock and value stock performance then and now — even after the debacle of the fourth quarter of 2018 — is extremely similar.

Does this mean that the relationship is about to make a marked shift, "normalizing" the valuation of growth and value stocks? There are no pre-established rules. There are tendencies, there are generalities, there are probabilities, and there is analogous history.

There are also differences in conditions between the two periods. For example, in 2000–01 many of the lower-volatility or defensive stocks such as utilities were historically cheap. Utilities today are near record high valuations, so one would not expect a repeat of the early 2000s.

As many academics have shown, and as any person on the street knows intuitively, future returns are inversely proportionate to starting valuations. Consider another classic defensive group, consumer nondurables, a group that has recovered from extreme cheap valuations, but is now suffering from evolving consumer taste and habits, competition, excess supply, and changes in distribution. It offers, as a group, fairly dim fundamental prospects without excessive "cheapness" to counterbalance that.

So with these disclaimers out of the way, let's take a look at some charts comparing the growth vs. value cycle over the past 5 years compared to the 5-year period ending on December 31, 1999.

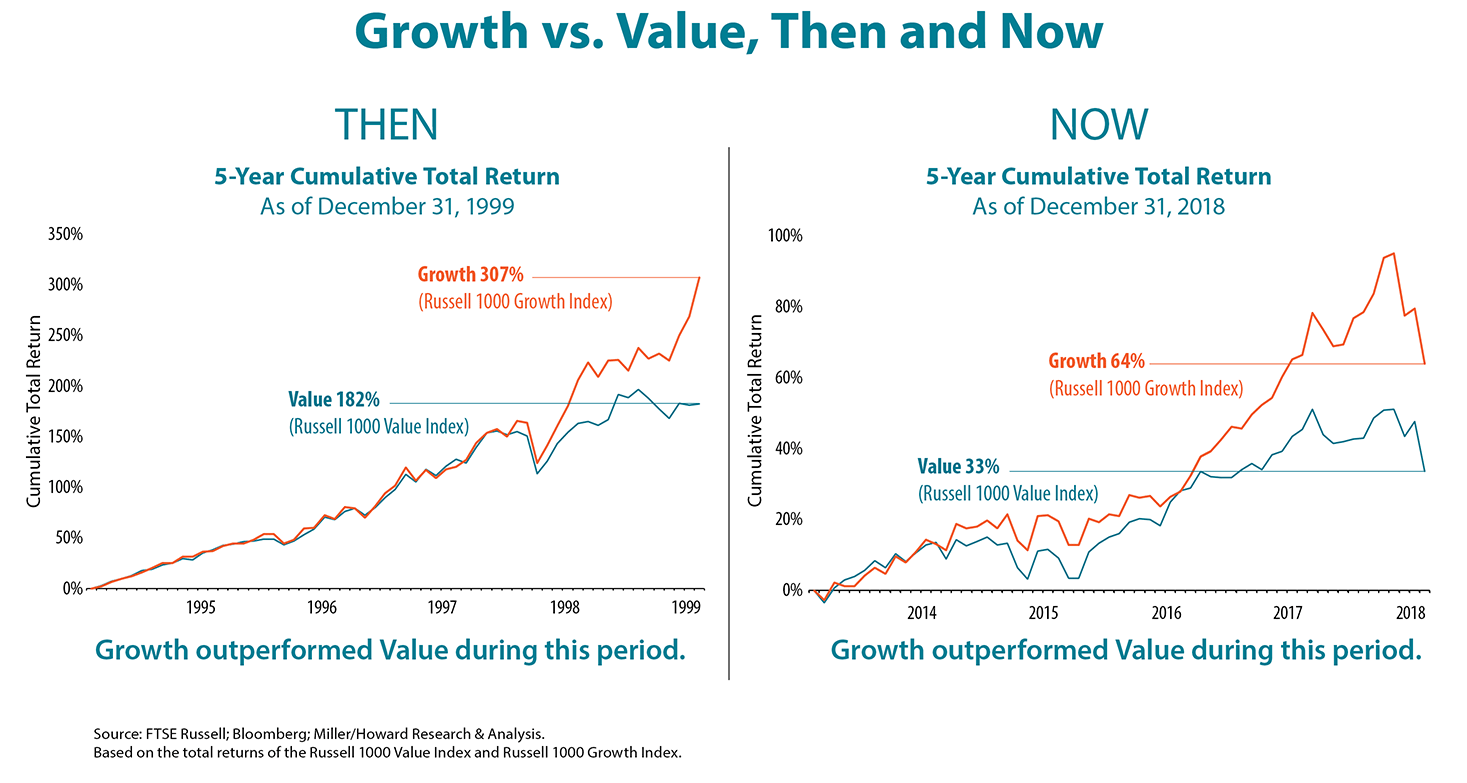

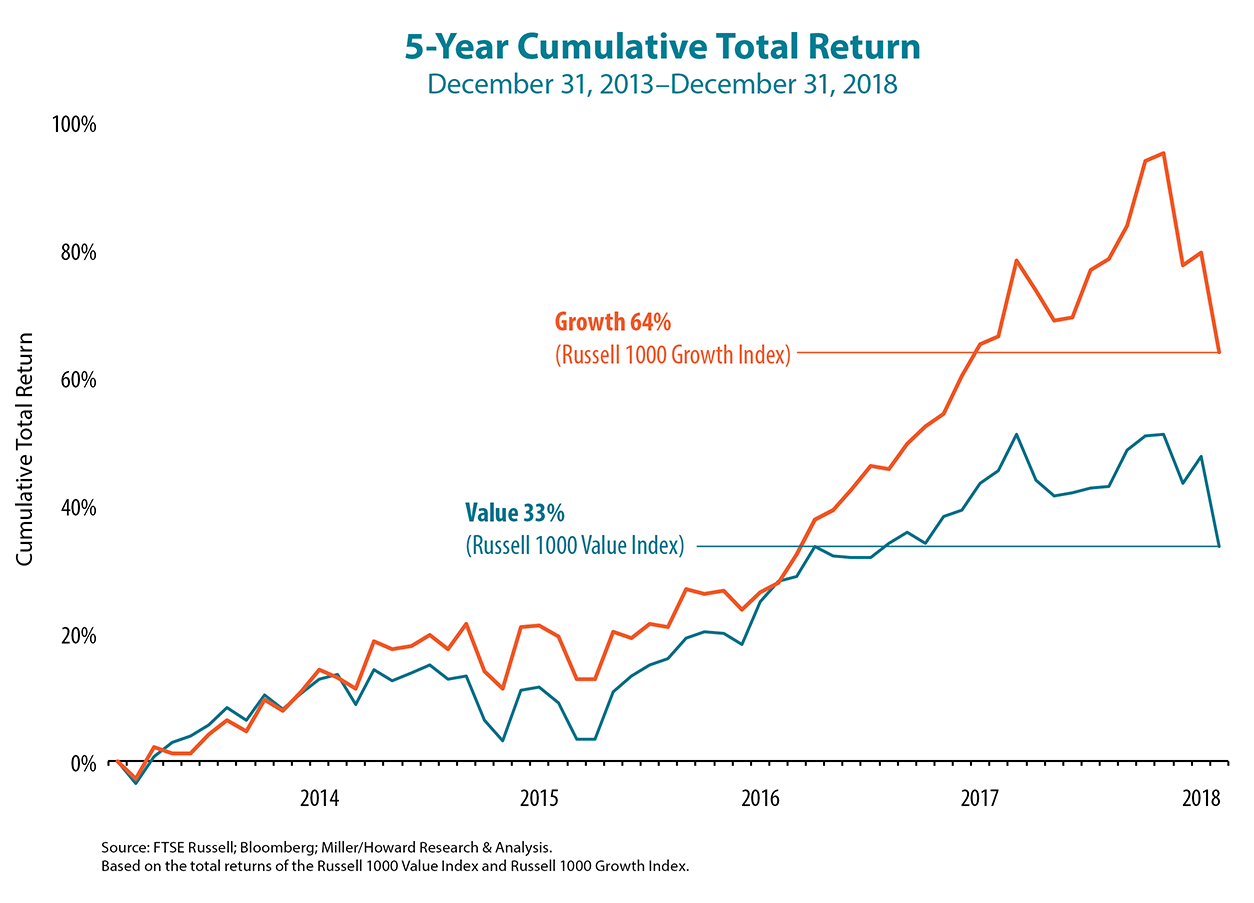

Growth has outperformed value over the past 5 years, with most of that outperformance occurring over the past 2 years.

We saw a similar environment at the end of 1999 when growth stocks outperformed value. Compare the 5-year periods side by side again — 5-year returns as of December 31, 1999 (THEN), vs. 5-year returns as of December 31, 2018 (NOW). Note that most of the outperformance in both happened over the last 2-year period of the time frame.

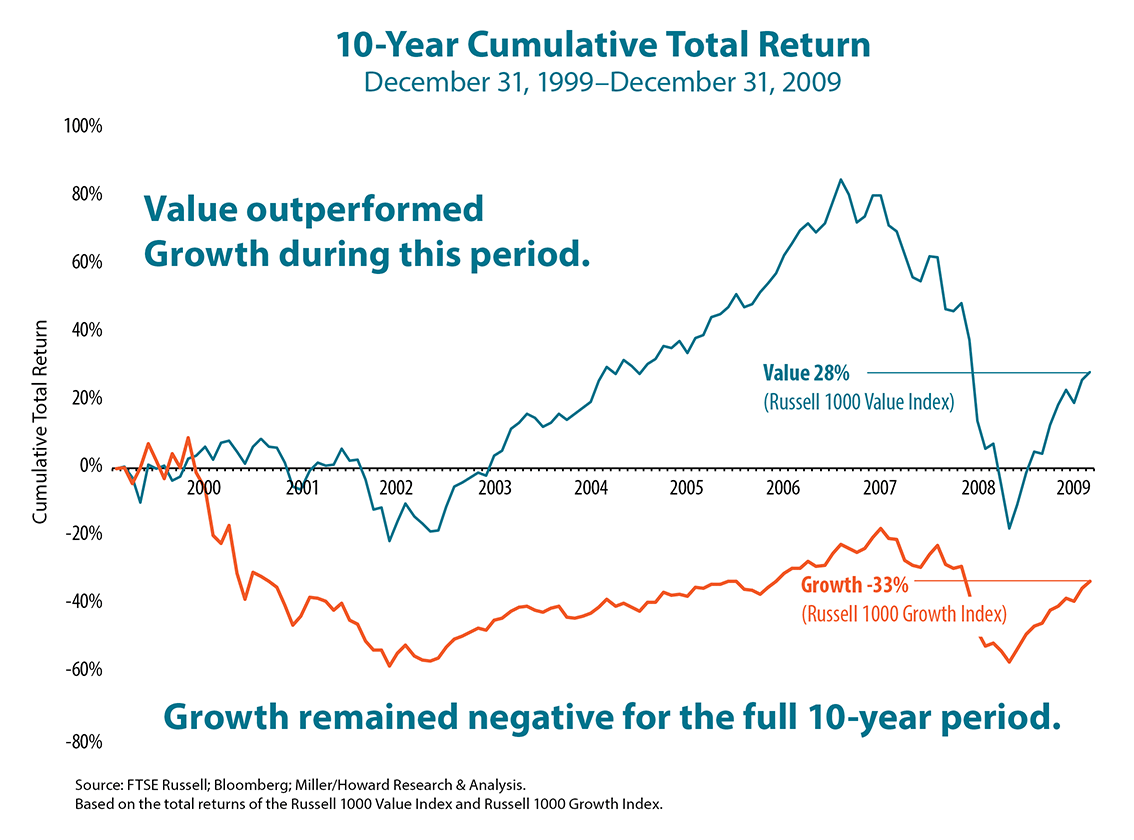

What happened after the trend reverted in 2000?

Below is a 10-year chart starting in the year 2000. Notice that the Russell 1000 Value Index turned positive by the end of the fourth year, while growth remained deep in negative territory. Growth returns remained negative throughout the 10-year period.

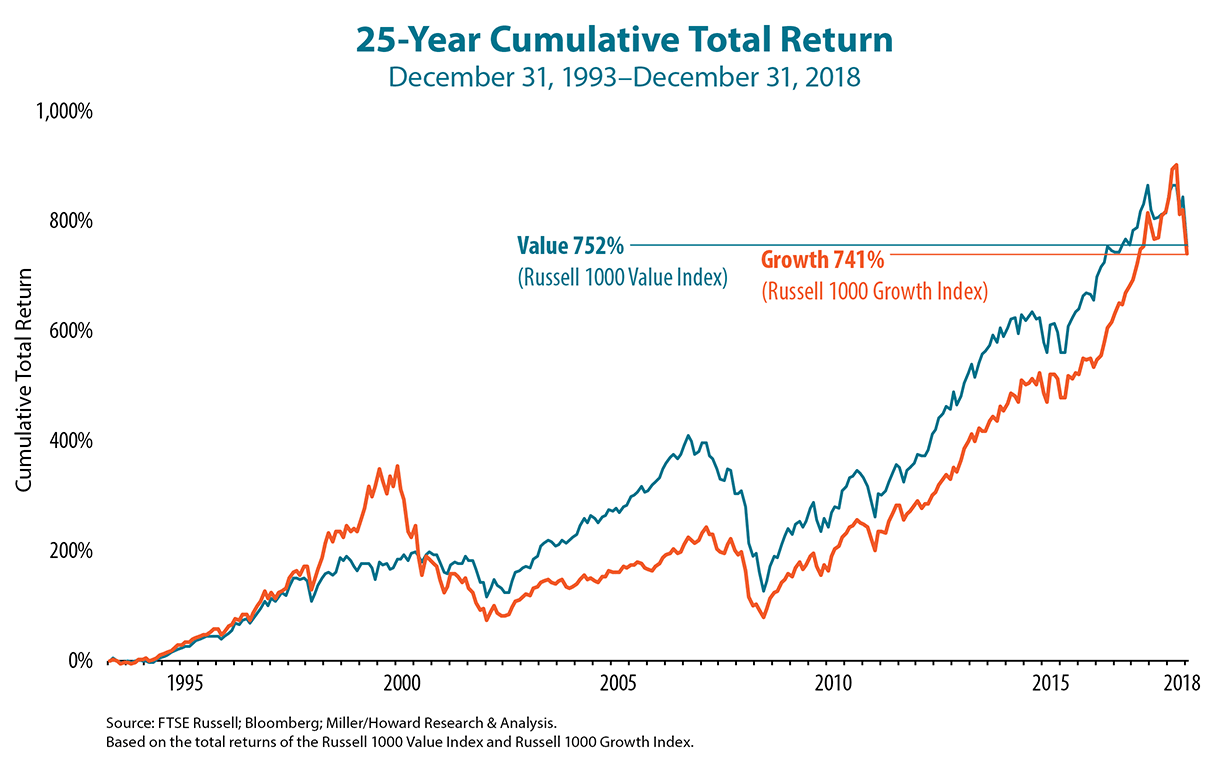

And here is the same chart extended to the past 25 years as of December 31, 2018. Despite including two periods of strong outperformance by growth stocks, total returns over this almost 25-year period are remarkably similar with growth only recently outperforming value.

Which leads us to make some general comments about interpreting market cycles. It's not to say that present flashes can't be reliable signals, but we believe it's more prudent to also consider longer-term cycles and market performance. The problem, of course, is that it is rarely obvious which signals could be indicative of future success.

As a result, we think it is important to understand your investments, create a long-term plan, and stay the course with your long-term goals and objectives.

Don't let market distractions steer you away from long-term success.