Income Stocks Are a Good Idea for Spenders

Wednesday, March 27, 2019

The first rule of spending is to save first. When it comes to spending, especially in retirement, conventional wisdom suggests that you “spend from total return.” In other words, you shouldn’t worry about whether returns are coming from appreciation in the price of your securities or from the dividend income these securities produce. After all, you can sell whatever you need to meet your spending budget.

A well-known principle in the retirement industry is the 4% Rule — which argues that you can spend 4% of the value of your overall portfolio, of course adjusting this value each year for inflation. History has shown that the stock market has gone up on average about 10%* annually in the last 5 years. So, the argument goes that the chances of running out of money appear to be slim.

What Could Possibly Go Wrong?

We all tend to make assumptions that may not hold true, and the real world is not always so neat and tidy.

To begin with, the logic above is based on percentages — but people don’t spend percentages, they spend actual money. They are not the same thing. If after the market goes down, and an investor sells principal to meet spending needs, that principal won’t be there to benefit when the market eventually goes up.

Let’s take an example:

- You start with a $100 portfolio.

- The market then falls 10% (very possible occurrence) = $90.

- And then you need to take the 4% of the original portfolio value for your spending needs. That leaves you with = $86.

- The next year the market hypothetically goes up 11% bringing the stock market roughly back to its starting point, your portfolio only goes back up to = $95.50.

- You were able to spend the $4.00 — but you have not raised any new money for the next year’s spending. That missing $0.50 is the cost of having to sell when the stock market is down, a sort of negative compounding!

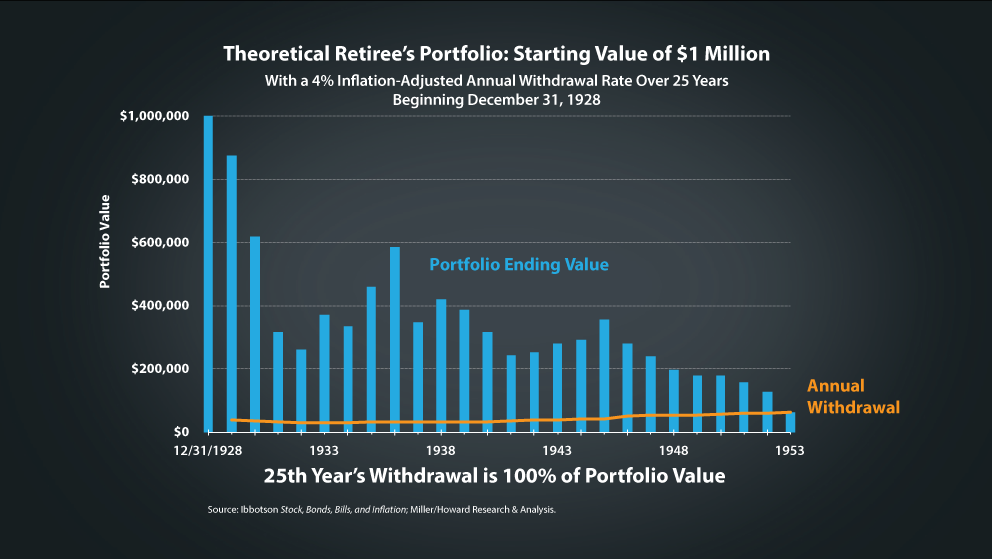

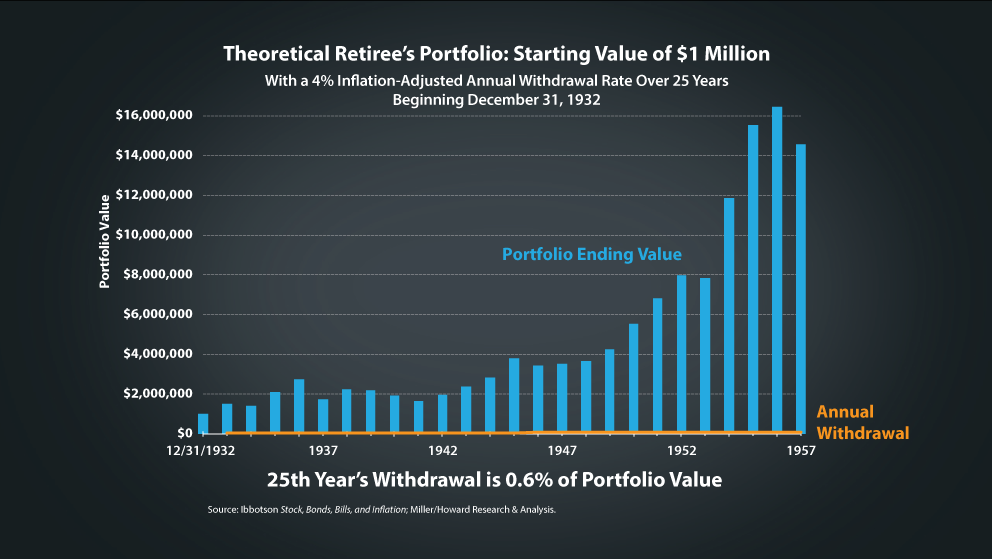

How well this rule works is very dependent on when you retire. Using Dr. Roger Ibbotson's long-term stock market returns, we constructed a model to see how this rule would have worked over a 25-year retirement, starting at various points of time. Our assumption is you started with a $1 million portfolio, and your returns are based on an investment in Large Company Stocks, as Ibbotson calculates them.

For the withdrawal rate, we assumed a 4% rate of the original portfolio value adjusted annually using the most widely quoted US inflation measure, the US government's Consumer Price Index for All Urban Consumers.

Let’s look at what turned out to be the worst-case scenario: retiring at the beginning of 1929. By the end of 25 years, the retiree had less than one year’s worth of spending left in the portfolio. The retiree ran completely out of money.

Now, if the individual, instead, retired just four years later in 1933, the outcome would have been dramatically different. At the end of 25 years, the retiree’s next withdrawal amount would have represented a minor 6/10th of 1% of their portfolio rather than the 100% in comparison to the person who retired in 1929.

That short four-year delay in retirement meant the difference between having $62 thousand or over $14 million 25 years later — between outliving their money or leaving their heirs with a sizable inheritance.

The main points we are making are:

- There are risks inherent in spending from total return versus the peace of mind that can come from spending out of a reliable and stable income stream.

- If you have a portfolio of high-yielding dividend stocks that can maintain their dividends, or better yet grow their dividends, you can spend out of the income that your portfolio generates.

- Then you won't need to sell when the market is down. You won't need to erode your principal when you need it most — to recover from a stock market decline.

- You won't need to worry about the market volatility as much because your spending needs are covered by the cash flows that your portfolio generates for you. Financial independence means being able to live off of your income.

* Does not include transaction costs, taxes, and fees.

DEFINITIONS

Ibbotson® Large Company Stocks Index is represented by the S&P 500 Composite Index (S&P 500) from 1957 to present, and the S&P 90 from 1926 to 1956.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Indexes are available for the US and various geographic areas. Average price data for select utility, automotive fuel, and food items are also available.

John (Jack) E. Leslie III, CFA, focuses on diversified, dividend-paying stocks. He is a member of Miller/Howard's Board of Directors. Prior to joining Miller/Howard in 2004, Jack was a portfolio manager at Value Line Asset Management, M&T Capital Advisors Group (a division of M&T Bank Corp.), and Dewey Square Investors Corp. (now part of Old Mutual Asset Management). Jack earned his BS in Finance from Suffolk University and an MBA from Babson College.