Keeping a Long-Term View of the Real Economy

Monday, March 30, 2020

In last quarter's report we offered ideas about how to make clear and rational decisions in the midst of the herd activity that surrounds the market. One of the key points we mentioned for avoiding herd emotion and herd action is to maintain a long-term view during times of stress. Today, we believe investors should be focusing not on the daily tally of "coronavirus case counts," but on how the real economy will most likely look in 3 to 5 years. From that perspective, many may find current market conditions enticing.

Recent Crises at a Glance

Since the founding of our firm in 1984, there has been an important crisis in the markets every 8–12 years (our founding coincided with the end of the oil-shortage crisis and the end of sharply rising interest rates in response to what had been out-of-control inflation). In 1987 there was a sharp crash that was mainly the result of secular market dynamics and not the real economy (portfolio "insurance" and program trading backfired as exit possibilities could not accommodate the magnitude of fleeing positions). Indeed, the real economy continued to do reasonably well, and markets slowly recovered as investors regained confidence that the system had been repaired. Perhaps that technical crash was also a precognition of the disasters for banks in 1990–91, when rising rates exposed the corruption in savings and loans banks and upended the mortgage market. But that was an economic hiccup, not really crisis.

After relatively smooth sailing during the Clinton-era 1990s, in 2000 the tech bubble of elevated "new economy" valuations collapsed. This was devastating to the portfolios of investors who were even partly invested in technology, but what was plain in real time became even plainer in retrospect. That is, the valuations of that sector bore no relation to sensible business valuations; they were pure emotion. Investment accounts were harmed, but so-called value, or "old economy," stocks began to rise as investors remembered what investing really is. Again, a crisis for investors and the trading marketplace, but not truly a crisis for the real economy. Not long after each of these "crises" the equity markets recovered and went on to make new highs within a reasonable investment time frame.

The year 2008 was a true crisis felt in the markets but also in the society at large. We can recall wondering if our economic system could survive. Banks were hurt worst, but the overall economy ground to a halt and unemployment soared. Would everything be different in the future? It turned out to be a slog, a long slow process that never really became robust. But that wasn't bad at all for investors, for new money at least. A famous investment firm coined the term "new normal," suggesting a poor economy and low future returns, demonstrating that even the most sophisticated investors and analysts can't always know what lies ahead. The "new normal" proclamation came almost to the day of bottoming for the market and the economy, in March of 2009.

The Crisis Right Now

Is this 2008 all over again? 2020 is a time of extremes, and it is uncertain. It isn't 2008 because the financial system has remained intact, and that's what's needed for economic recovery. But it isn't a trivial moment, to be sure.

Volatility is extreme by any measure. One has to go back to the 1930s to find analogs. Volume is equally extreme. Sentiment measures are extreme. Debt levels are extreme, and that's not a good thing in a time of reduced cash flows. But like 2008, the government has gone into action to protect the economy. Observers were skeptical then, but we were skeptical of the skeptics, and expressed a longer-term optimism because the government was "on the case." Yes, it was an anxious time, and we feared for banks as the linchpin of the financial system, but slowly the various financial and fiscal programs gained traction, leading to one of the most durable bull markets of the modern era.

Some Positive Points

There is much we don't know, including the duration of the pandemic (as we write at the end of March it shows no signs of abatement in the US or Europe). However, we have faith in our medical industries to eventually solve this problem—after all, hepatitis C, a virus, has been cured, and HIV, also a virus, has been effectively suppressed. The relevant scientists suggest that either cure or vaccine or both will be available within about a year or less.

The medical crisis will pass. The question is how much damage will it do to the economy during its period of acute infection? That is not something anyone can know at this point, but we suspect its reach will be broader and perhaps deeper than 2008. That doesn't mean it will be worse for investors, since stocks tend to discount a recovery long in advance of reality. And banks, the aforementioned linchpin of the economy, are profoundly sounder than they were in 2008. The tools to restart stability and growth are there.

The President was right that our economy is "not built" to shut down. Americans want to be out there working, producing, and striving. That's all true, but our understanding is that the US economy is "not built" to withstand periods of zero revenue. That will deal a body blow to retail-facing industries such as the stores and restaurants that are closed as we write, and all who supply and service them, as well as the debt financers who enable the whole chain of commerce.

A glass-half-empty view posits that the economy has suffered a disruptive body blow, the microbial equivalent of a hurricane that flattens a town. However, a glass-half-full view asserts that the town has been flattened before, and it has rebuilt before, with better and new buildings that are hurricane proof. Over 250 years the system and the people within it have shown resilience, tenacity, determination, and imagination—and have always come back. We don't see why this will be any different, though the human toll in terms of mortality as well as economic disruption will be great.

The Short-Term Fallout

Like many things, however, the doing will be harder than the envisioning. There will be personal tragedies and business tragedies. The government will be poorer and deeper in debt, and taxes will eventually have to rise. Interest rates may not be as benign as they were after 2008—recall that the vast consensus of observers then predicted higher interest rates, though that was wrong because so much liquidity overwhelmed the demand for money. And there will be changes in society as well as the economy as a result of the pandemic.

On the downside, we think the universe of retailers and restaurants will substantially shrink, as will the population of workers in those industries (roughly 20 million before COVID-19 hit—about 100 times the average new claims for unemployment for 20191). Landlords will share the pain, both for commercial tenants and individual renters. Companies with substantial debt will find themselves unable to cover their monthly payments. In a restrained economy there is less need for resources, including energy and minerals, and for the tools and equipment of extraction and processing.

The Upside for Investors, as We See It

On the upside, life in the cloud has proven itself. Work from home will gain new traction, and 5G services will meet accelerated and increased acceptance. Everything cloud acquires new urgency. Much will go on as before, especially for the healthcare industries serving an aging population. Technology was a kind of savior after 2008, and its efficiency and productivity mean it will continue to play that role. And of course you have to turn on the lights, and run that technology, so utilities need to remain an important factor in an investor's landscape.

Secular market factors are very positive, and if not for the uncertainties of the pandemic they would suggest the best opportunity to invest in equities in at least a generation. Volume has not been so high since 2008, and high volume typically marks the end of a decline. Prices have declined sharply. Enough to discount the harder road ahead? That's unknown, but the further prices decline, the more they discount negative prospects. Sentiment has swung from an extreme of bullishness (which is bearish) to an extreme of bearishness (which is bullish). Stocks are oversold by quantitative measures, a reasonably expectable bounce at the end March notwithstanding. Rates remain low and will likely stay that way for years, at least at the short end.

The Fed is ready to do "whatever it takes," and the previous episode of this posture worked out well for equity investors—there will be no shortage of money, which may overcome inevitable low velocity. Because bonds rose this year and equities declined sharply, large institutions (including pension funds and sovereign wealth funds) around the world with an equity/bond mix will need to rebalance in favor of equities, and that is a huge source of funds for the equity market. A record-breaking flow of funds into money markets and short-dated credit will want a new home before too long, as returns of less than 1% get tiresome when you have a mid-single-digit or higher return assumption for your funds. Private equity is loaded with cash to purchase whole companies.

Will the two themes—economic damage and uncertainty as to duration versus a classic setup laying the groundwork for a new bull market—balance out? No one can know without more data and information, but the environment is not all one-sided.

A Future for Dividends

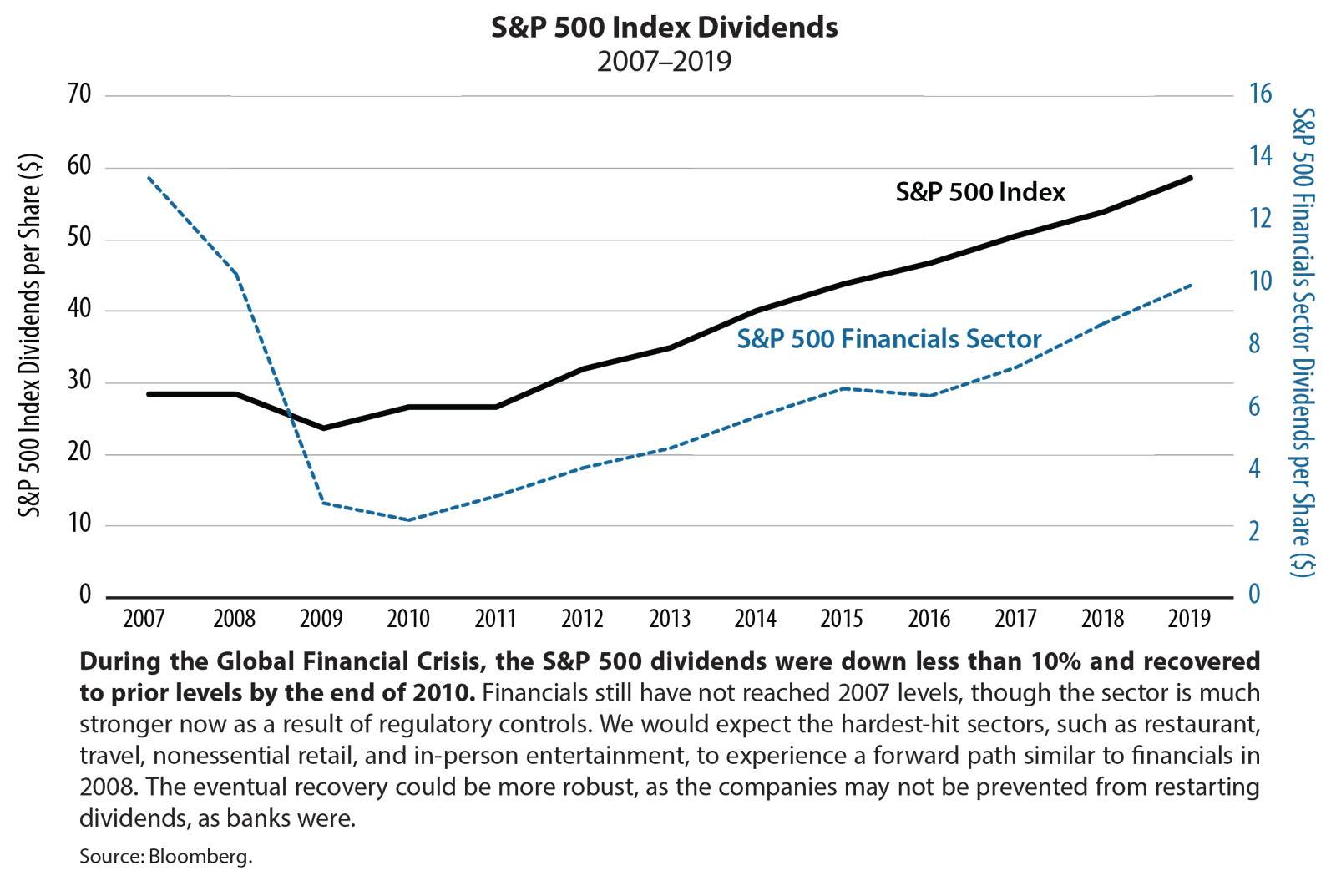

Importantly for us, we are well aware that dividends are not guaranteed. Companies whose cash flow has disappeared are not going to have the funds to pay dividends (which should always be an evidence of prosperity in any event), and we will see many reductions and cuts in the broad market, just like 2008–09 (1 out of 3 S&P 500 companies cut in 2008–9, though aggregate levels were restored by about 3 years out). Some companies will take action out of a feeling of prudence due to uncertainty, even if they can in fact afford to keep paying.

All of our strategies have high dividend yields—typically in excess of four times the yield on government bonds—and we want to keep it that way. We've focused for decades on companies with reliable cash flows and strong balance sheets that can ride out a period of softness, and these special times alert us to increase our vigilance even further. Of note, the many dividend-oriented "products" or "indexes" that have arisen in recent years are driven by formulas relating to past dividends, but pay little heed to balance sheet strength or current conditions that may impact the dividend. In other words, those portfolios are carrying lots of securities that met the criteria in 2019, as of the last index rebalance, but may enter the ranks of nonpayers in 2020. Our efforts are dedicated to distinguishing our portfolio from those passive approaches and keeping the income high.

It is our philosophy that long-term investment success depends on reliable income, and for us, nothing has changed. We will always adapt to current circumstances when necessary, but our foundation remains the same. Now more than ever, a long-term view gives us comfort in the resilience of the real economy.

Lowell G. Miller founded Miller/Howard Investments in 1984. Lowell has served as President and Secretary of Miller/Howard's Board of Directors, as well as President (Principal Executive Officer and Trustee) of Miller/Howard High Income Equity Fund, and Chairman of the Board of Trustees of Miller/Howard Funds Trust, since the funds’ inceptions in 2014 and 2015, respectively. He began his studies of the securities markets as an undergraduate and has continuously pursued the notion of disciplined investment strategies since 1976. He is the author of three acclaimed books on investing, including The Single Best Investment: Creating Wealth with Dividend Growth (Print Project, 2nd Edition, 2006). He has also written on financial topics for The New York Times Magazine, and has been a featured guest on Louis Rukeyser's Wall $treet Week and Bloomberg TV. Lowell is frequently quoted in financial media such as The Wall Street Journal, Dow Jones Newswires, Bloomberg, Fortune, and Barron's. He holds a BA in Philosophy from Sarah Lawrence College and a Juris Doctor degree from New York University School of Law.