Our Positioning in the 2020 Pandemic

Monday, April 06, 2020

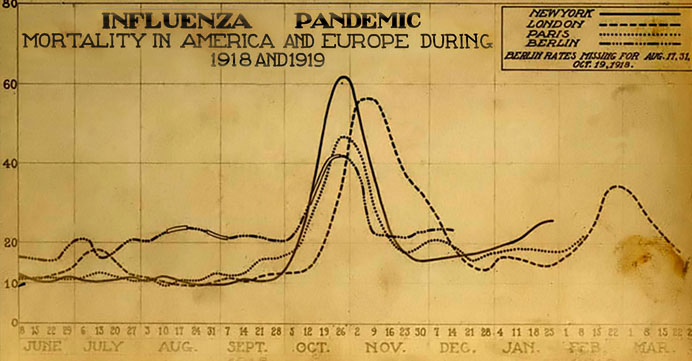

The Spanish Influenza. Chart shows mortality from the 1918 influenza pandemic in the US and Europe. Courtesy of the National Museum of Health and Medicine. This work is in the US public domain as it was published or registered with the US Copyright Office before January 1, 1925.

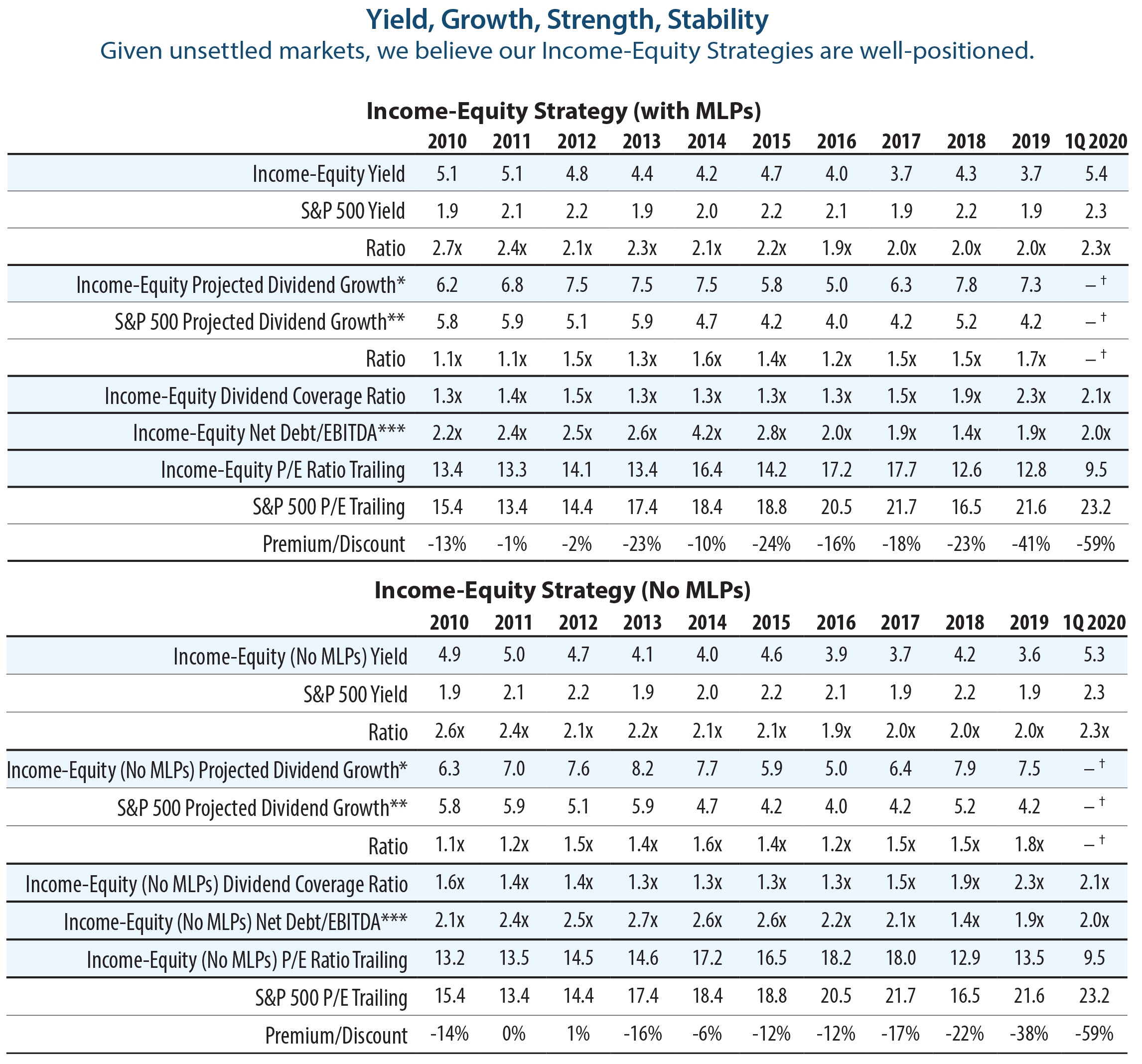

- The Income-Equity strategies each offer a high dividend yield that is 2.3x the yield on the S&P 500 Index, and our strategies have ample dividend coverage and reasonable leverage levels (net debt/EBITDA).

- Both portfolios trade at a significant discount to the broad market on price-to-earnings as well. Value investing historically has done best coming out of a recession, so the historically low valuations should set the Income-Equity strategies up for a strong recovery, in our view.

- The near-term picture is cloudy for projected dividend growth. However, we believe the portfolios are well-positioned to weather this downturn and poised to return to dividend growth when economic conditions improve.

When discussing extreme weather events, you'll frequently hear people joke that 100-year events, say floods or hurricanes, are coming every five or ten years. But in the case of pandemics, extreme outbreaks are truly rare.

One hundred years ago a vicious strain of influenza engulfed the world. Estimates of the death toll vary widely, ranging from 20 to 100 million in a much less populated world. We have better medicine today, but human nature hasn't changed much. Skepticism among politicians and businessmen was rampant: Why shut everything down? What's a little flu? Looking back, it's easy to second-guess those who wanted life to go on as normal. Few events in our experience can unfold as fast as a pandemic.

However, the pandemic will end in a time frame that is short for a long-term investor, and the ultimate value of our investments will be largely unaffected, in our view. This may sound like a throw-away comment, but it's actually very important. If we were investing in sports franchises, this conclusion would not hold. Suppose a basketball team loses its star center. That would put a permanent dent in the value of the franchise. For a large corporation, there is no equivalent. It would be sad if the CEO of one of our holdings was unable to work because of the virus, but a competent CEO should have a succession plan and business should run as usual.

The pandemic will permanently impact some businesses. The most obvious are idiosyncratic—for example, consumers may shy away from cruise ships for years. Most of the long-term economic damage, however, will be associated with problems faced by overly leveraged companies. Getting from the current state of emergency to the other side will involve challenges, including lower revenue, disrupted supply chains, difficulty collecting on debts, and the like. Companies with variable cost structures will likely contract and then expand again with little permanent damage. Highly indebted companies could have trouble, both paying their interest cost as well as finding a willing lender if they need more capital to get through the valley.

In contrast, firms with healthy balance sheets should have the flexibility to survive the crisis and thrive on the other side. Through our process of intensive due diligence and continuous monitoring, we're confident that these qualities predominate in our portfolios relative to their respective categories.

For example, we continue to focus on high current yield, prospects for dividend growth, financial strength, and earnings stability in our Income-Equity strategies. As the charts below show, we believe the companies in our Income-Equity strategies are well-positioned to weather this downturn and poised to return to dividend growth when economic conditions improve.

Source: Bloomberg; S&P 500; Miller/Howard Research & Analysis. The data above is based on representative accounts in our Income-Equity Strategies both with and without MLPs and is subject to change. Dividend yields shown for Miller/Howard portfolios exclude cash. All data is as of year-end, unless otherwise noted.

* Projected Dividend Growth—Miller/Howard Portfolio Team's 3-year annualized projected dividend growth based on data from various sources, adjusted to reflect our view of future economic and market conditions. There is no assurance projections will be realized.

** Bloomberg Dividend per Share 3-year forward estimates.

*** Excludes financials.

† 1Q 2020 projected dividend growth has been removed due to the unreliability of current projections within the current environment. The 1Q 2020 earnings season should provide clarity regarding projections.

Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA)—A non-GAAP measure used to provide an approximation of a company's profitability. This measure excludes the potential distortion that accounting and financing rules may have on a company's earnings; therefore, EBITDA is a useful tool when comparing companies that incur large amounts of depreciation expense because it excludes these noncash items, which could understate the company's true performance.

Net Debt to EBITDA—A measure that computes the company's ability to pay off its debt by utilizing the earnings before interest, taxes, depreciation, and amortization (EBITDA).

Price-Earnings Ratio (P/E)—The ratio of a company's share price to its earnings per share. The ratio is used as a valuation tool and can help determine whether a company is overvalued or undervalued.

Emeritus CIO