Proxy Voting: An Investor’s Right and Responsibility

Monday, July 06, 2020

Investors have an opportunity to provide opinions and oversight to companies they hold, and we believe that strong corporate governance requires sensitivity to the views of shareholders.

Investors have an opportunity to provide opinions and oversight when a company holds its annual shareholder meeting. The meeting agenda, often available in the proxy statement, features a variety of ballot items (called resolutions or proposals) on which investors are asked to vote. These may include ratification of independent auditors, advisory approval of executive compensation plans (Say-on-Pay), election of directors, and yes or no votes on shareholder proposals. Voting on these is the right of every shareholder.

For each item on the ballot, management will typically issue a voting recommendation. It is widely known that management generally recommends that investors vote FOR whatever resolutions it has put forward, and AGAINST resolutions shareholders have added to the ballot.

Management’s recommendations may very well be sound and fully explained in the proxy statement. Nevertheless, Miller/Howard strives to prioritize investor interests above management’s recommendations. We actively review and vote each item on the ballot according to what we believe best serves our clients.

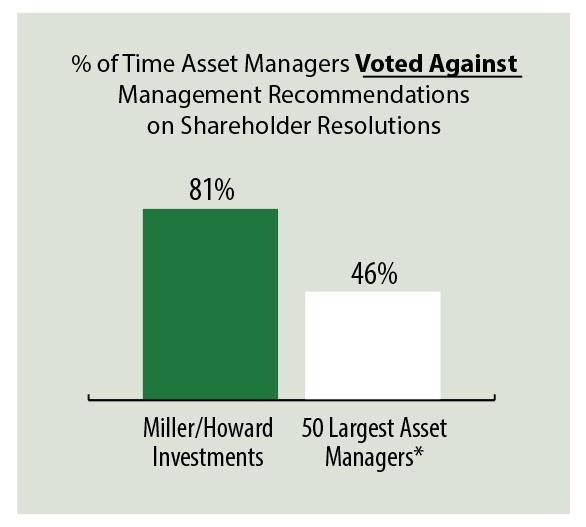

Accordingly, Miller/Howard finds itself sometimes voting against management recommendations. Many other investment managers vote with management more frequently, as the chart on the following page shows.

- Each annual meeting, investors have an opportunity to provide feedback to management. Investors can rubber-stamp management’s recommendations, or they can vote actively and according to their own interests.

- Miller/Howard reviews each ballot and votes based on our view of what’s in our client’s best interest. In the example above, we voted against an executive pay package (there was a pay/performance disconnect), and for a shareholder proposal that seeks greater transparency around a company’s management of environmental issues, such as emissions and climate change.

- You can see where management told us to vote one way and we voted another, and also that we sometimes vote with management recommendations.

Why Vote against Management?

Here are some examples:

- We believe a report on climate risks would serve the company and its shareholders well. We would then vote for the shareholder proposal, when management suggests we vote against it.

- Insufficient gender diversity on the board, which can speak to the style of governance as well as the company’s approach to competitive recruitment and positioning. We would vote against directors on the nominating and governance committee.

- Pay and performance disconnect. We would vote against the advisory Say-on-Pay proposals, which communicates shareholder opposition to the company’s executive compensation package.

But it’s not just about the vote: A company’s response to the vote can indicate the quality of management. While many, if not all, of the items on a proxy ballot are considered advisory—e.g., information for management but not binding on their actions—we believe that strong corporate governance requires sensitivity to the views of shareholders. If a substantial number of investors vote against the company’s executive compensation program, management should consider this both actionable and material feedback. If a company chooses to ignore such messages, it can serve as a lesson and a warning for investors.

Votes cast at meetings that took place in FY 2019.

Source: Morningstar; Miller/Howard Research & Analysis

*Based on the percentage of proxy votes that were voted contrary to Management’s recommendation, averaged across 50 large fund families, as calculated by Morningstar based on its Proxy Data.

Learn more in our Shareholder Advocacy & Engagement Report

Nicole Lee provides operational and strategic leadership to Miller/Howard's ESG team. Nicole’s ESG research on portfolio holdings and candidates is integral to the firm’s investment process. Prior to joining the firm in 2014, she worked for several years as a clinic coordinator and educator for a nonprofit health organization, during which time she also developed and conducted training programs at two local universities. Nicole received a BS in Sociology from Southern Utah University, after which she studied public health at Westminster College in Utah.