Shift Towards Value Continues

Monday, April 12, 2021

The news coming out of Pfizer’s vaccine trials on November 9th was truly spectacular and triggered a meaningful shift in the stock market.

The news coming out of Pfizer’s vaccine trials on November 9th was truly spectacular and triggered a meaningful shift in the stock market.

Value Outperformed Growth Post-Vaccine Announcement

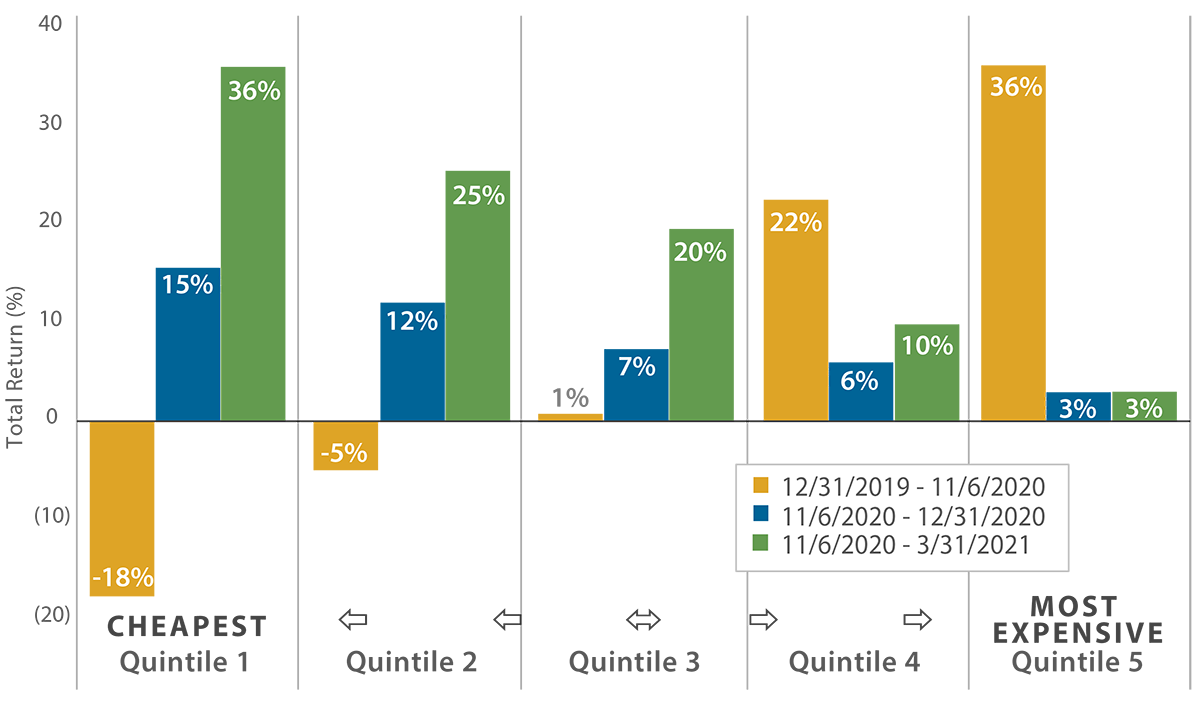

Performance Pre- & Post-COVID Vaccine Announcement (S&P 500 Index Forward P/E Quintiles)

As of March 31, 2021. Source: Bloomberg; Miller/Howard Research & Analysis.

As we noted last quarter, announcement of Pfizer’s successful development of a COVID-19 vaccine caused investors to lose some of their infatuation with expensive stocks and move towards the value side of the market. When we made that observation, we were admittedly commenting on a short period of time, roughly seven weeks. Now that 20 weeks have passed, we can say with more confidence that the market has indeed changed course.

The chart above shows the performance of stocks split into price/earnings (P/E) quintiles at the beginning of 2020. Prior to the vaccine announcement in November 2020, the more expensive the quintile, the better the performance. Our interpretation is that investors, prior to any proof that a vaccine would work, were more willing to pay for the growth stories of expensive stocks rather than the cheaper earnings and dividends of value stocks. Essentially, investors thought there was no “bird in the hand” option given the uncertainties of the pandemic, so they might as well pay up for mega-cap growth stocks.

Following Pfizer’s vaccine news, the market did a full reversal—the cheaper the quintile, the higher the investment returns. The vaccine news gave investors confidence that they could rely on the near-term earnings forecasts and dividends that make value stocks attractive. Of course, we have seen continuing good news since November 9th that helped keep the value rally alive, including additional vaccines authorized in the US and globally. After a sluggish start, US vaccination numbers began to surge in February, and it was announced that all American adults would be eligible for vaccines by April 19th. We also have seen COVID-19 cases drop from 2020 highs and the unemployment rate continue to fall. These are still not the best of times, but enough is going right for confidence to rebound.

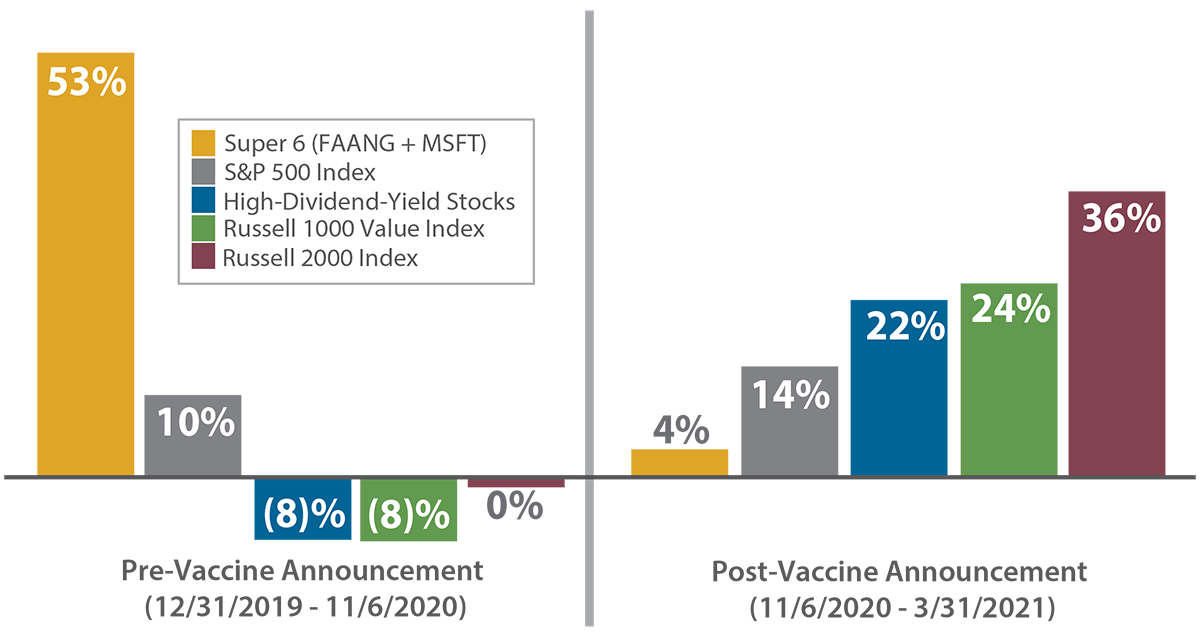

Performance Pre- & Post-Vaccine Announcement

As of March 31, 2021. Source: Bloomberg; Miller/Howard Research & Analysis. High-Dividend-Yield Stocks consists of Decile 7, 8, & 9 of a universe of US dividend paying common stocks with a market capitalization or greater than $4 billion. FAANG + MSFT= Facebook, Apple, Amazon, Netflix, Alphabet (Google), & Microsoft.

Vaccine news did more than shift the market towards value. The graph above shows other indications of investors shifting away from mega-cap growth stocks towards equity categories that have struggled in recent years. Stocks dubbed the Super Six, Facebook, Apple, Amazon, Netflix, Alphabet, and Microsoft, outperformed the market massively during 2020 prior to the vaccine news. The Super Six somehow morphed from stocks with exciting long-term growth stories to places to hide your money when it seemed like the pandemic would never end. Since the vaccine news, the Super Six have trailed the broader market.

Value, Dividend Yield, and Small Cap Rotation Continues

Since the vaccine news, the S&P 500 Index has continued to perform well, but the drivers of market performance are now value stocks and high-yield stocks. The recovery of small-cap stocks has been the most dramatic with the Russell 2000 Index up over 35% since the vaccine news.

The story on small-caps is a bit complicated:

- The small-cap universe is tilted towards cyclicals, so the value shift we saw in large-caps benefitted small-caps even more.

- We also saw growth investors move away from the mega-cap growth stocks towards small-cap growth stocks.

The rebound in small-caps is a good sign for both value and active management. Portfolio managers can, once again, be rewarded for sifting through long lists of potential investments from a wide range of market capitalizations, including stocks with good earnings and dividends that have been underappreciated by the market.

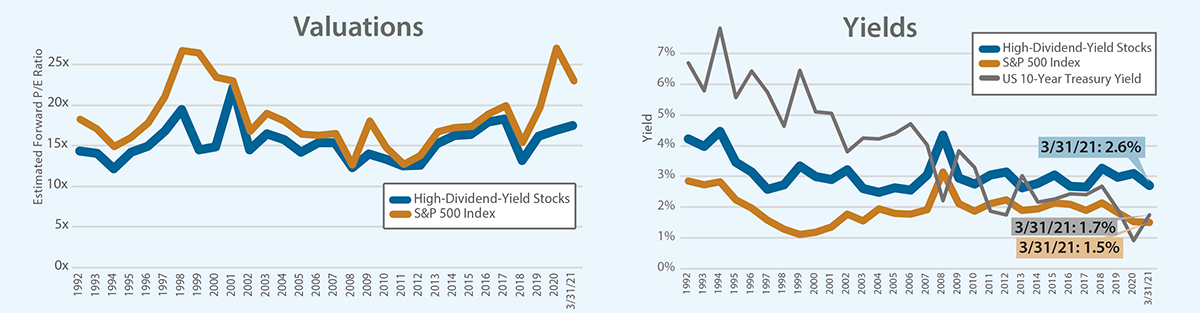

High-Dividend-Yield Stocks Are Trading at a Valuation Discount While Offering a Significant Yield Advantage Relative to History

As of March 31, 2021. Source: Bloomberg; Miller/Howard Research & Analysis. High-Dividend-Yield Stocks consists of Decile 7, 8, & 9 of a universe of US dividend paying common stocks with a market capitalization equal to or greater than $4 billion.

Despite the recent rally, the universe of high-dividend-yield stocks remains attractive relative to both long-term bonds and the broad stock market, in our view. The graph above shows how P/E multiples and yields have varied over time, using a wide-range of market capitalizations for the high-dividend-yield universe. The spread in both yields and valuations of high-dividend-yield equities versus both the S&P 500 and long-term bonds remains high, suggesting a good entry point for investors considering high-dividend-paying stocks.

Read the 1Q 2021 Quarterly Report ►

Emeritus CIO