The Popular Kids — Least Likely to Succeed?

Monday, April 15, 2019

As it was in high school, so it is today — the popular kids get all the attention. And as it was after high school, so it is in later life — the “most likely to succeed” often don’t.

Roger Ibbotson, originator of the seminal long-term study of financial asset classes, Stocks, Bonds, Bills, and Inflation, is at it again. This time, he and some colleagues have published a book-length study distributed on the CFA Institute website entitled, Popularity: A Bridge Between Classical and Behavioral Finance. Despite its dry, academic style, this arduous read has worthwhile (And might we even say “fun”?) insights for investors.

Here is its big idea.

In the classical model of finance, investors look for the conventional factors that are reflected in stock price, such as market risk, with each stock priced for its likelihood of realizing that risk, or avoiding that risk through such characteristics as strong balance sheet, safe dividend yield, or expected growth in cash flows over time.

But there’s also a behavioral finance model of finance that colors investors’ decisions. Ibbotson et al. say that “asset prices should also reflect the characteristics that investors like ‘too much.’ Stated simply and broadly, if an asset has characteristics that investors really like, its price will be high. If it has characteristics that investors do not really like, its price will be low, all else being equal. Thus the asset with the more desirable characteristics should have lower expected relative returns, whereas the asset with less desirable characteristics should have higher expected relative returns.”

They found, through an exhaustive process of analysis involving multiple rankings, studies, and surveys, that the more popular the stock, the less likely it is to succeed.

The Popularity Model of Pricing

“Popularity” indeed does seem to unify the mechanistic classical theory of the Capital Asset Pricing Model (CAPM) with the more fluid, dynamic, and contextual character of behavioral finance. In effect, classical theory shows why markets are efficient because market participants are rational, and the set of “popularity” characteristics the authors identify shows why markets are not efficient because market participants are not rational — or at least not entirely so. In this case, we need to acknowledge that both are right. This is what Hegel called the “dialectical unity of opposites.”

Ibbotson et al. wanted to know what character set could define the real-life application of behavioral finance principles, and came up with a companion or complement to the CAPM, which they call the PAPM (Popularity Asset Pricing Model). PAPM focuses less on purely rational pricing elements, such as the estimated growth in cash flows, and more on the demand for different features coming from different investment constituencies. Because stocks have different categories of features that are more and less in demand — whether sustainably so or temporarily — the excess return stocks can earn varies far more widely than a CAPM analysis would predict.

The PAPM asserts that, “Investors have differing risk aversions and popularity preferences. The characteristics are priced according to the aggregate demand for each of the characteristics. The expected return of each security is determined by its risk and popularity characteristics.” To us this is only common sense, and is reminiscent of Buffett’s well-known comment that “in the short term the market is a voting machine, and in the long term the market is a weighing machine.”

The nut of PAPM is that in the short term there are features that make stocks “popular,” but in the longer term popularity yields poorer results — because those features have already been discounted and priced in by the time a stock reaches the status of “popular.” Many studies have shown that expected forward returns for the overall market (whose risk dominates all securities) are lowest from points of highest valuation, or popularity.

5 Popularity Factors that Predict Returns

That’s historical fact, but the Ibbotson group wanted a predictive model. Thus, they identified five characteristics of stocks that make them “popular” to see how these popularity factors may have predicted their returns (relative to all else), in advance.

- Brand. Most of us are more comfortable with companies that have high brand values. But, using a variety of surveys and polls to establish brand value, they found that the quartile of companies with the most respected, or popular, brands ended up having significantly lower returns than the quartile of companies with the lowest brand value (for the 2000–2017 period).

- Moats. Companies with sustainable competitive advantages, or “wide moats” (using Morningstar evaluations), are thought to have an edge over the long term, since they have pricing power. Thus, “wide moats” are popular. But again, wide-moat companies underperformed no-moat companies in the period 2000–2017.

- Reputation. Like people, companies with high reputations (using surveys and rankings) are popular among investors. However, high-reputation companies underperformed those with poor reputations, 2000–2017.

- Low tail risk. Assets with low tail risk — that is, they move much less than average from their median price — are popular because they act more like the market with which investors are familiar. However, the quartile of stocks with historically high negative tail risk (severe and abrupt declines), generally thought to be unpopular, outperformed low tail risk stocks, 2000–2017.

- Lottery-like characteristics. Stocks with high price targets and high recent price gains are popular because they provide an apparent opportunity for outsized gains. However, these stocks provided the lowest risk-adjusted returns during the study period.

Less Exciting Has Become More Desirable

Ibbotson and his coauthors also studied the somewhat more conventional and numeric factors of beta and momentum. Like others before, they found that both of these factors provided excess returns — even though these are contradictory to the rationalist CAPM, whose central tenet is that return is directly proportional to risk. Lower beta, suggesting lower risk, provided higher absolute and risk-adjusted returns. Positive momentum was the same — though that effect would wane if momentum were so strong as to be “lottery-like.”

In effect, the Ibbotson group has provided the theoretical framework and some of the direct testing behind the “low volatility” strategic approach that has been so successful in recent years — which has, ironically, become very popular. Odd, since it is really a contrarian approach.

They point out that many active managers have focused on higher volatility stocks, the managers reasoning that since markets go up more often than not, higher volatility stocks will eventually give them excess performance. Thus, for long periods, especially those where hot growth stocks grab the headlines, lower volatility stocks will become unpopular and priced low relative to their “rational” CAPM values. Thus, the less exciting stocks end up providing better returns.

Our Own Takeaways

- Stock prices are set both rationally and emotionally. Almost from our first introduction to the markets it became clear that stock prices are set both rationally and emotionally, with an emotional band at about plus or minus 25% beyond an expected price derived from earnings, yield, financial reliability, and estimated future growth. How else can you explain the fact that both prices and PEs fluctuate for nearly every stock in a range of at least 30–50% every year, even though hardly any companies show fundamental change more than plus or minus 10–15% in any given year?

- Prices depend on demand. Obviously, and giving the lie to anyone who claims to know precise over- or undervaluation at any given time, prices depend on demand. It seems simple, yet it’s a principle often forgotten by those who are so busy counting the beans they fail to see the real world in front of them, or behind the numbers, as it were.

- Stock prices in general stem from demand for equities. This demand may originate in very bullish views about long-term prospects for the economy, or, as in our present moment, demand may arise almost defensively when the other available investment options present little appeal.

- It’s hard for us not to like popularity factors. After all, we are investors, with all the insecurities of investors (in a world whose future is ultimately unknown), and darn it, we would like our investments to have high brand value, because we view brands as never adequately valued in a stock’s price. We would like to have a wide moat (we grew up on real estate and utilities!). We have demand for a high reputation; we want to count on top management and the company’s ability to retain its customers. Yet it turns out, apparently, that all these “popular” characteristics have been discounted or arbitraged away as the company proceeded on its slow march to moatiness, brand royalty, and high reputation. Could it be that we weren’t the first or only investors to recognize these features?

- The missing factor is “improvement,” in our view. Could it be that what yields excess returns for investors is a company’s improvement rather than its demonstrated success? It’s true. It feels good to own a proven hero. But take care to avoid becoming like one of those baseball teams that pays a lot for an aging all-star, only to find he grows tired and injured. In practical terms, good investments will have some degree of aversion in the marketplace, giving them a moderate current price and ample room for improvement. Improvement may convert investor disdain to investor demand over time.

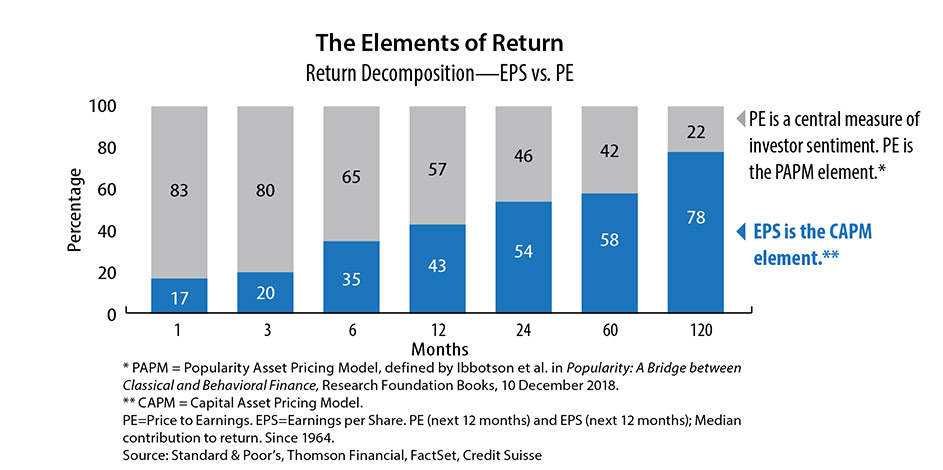

- Much of equity pricing can be attributed to changes in sentiment. Investors will pay different valuations for the same thing, depending on how they feel and how strong their demand is at any given point in time. Consider the chart. In the past five years about half of returns have come from increased demand, as measured by PE elevation. To be sure, low interest rates and Fed pump-priming may have increased demand, but it is still demand, resulting in price change. Over the past decade investors remained averse to the risk of stocks, as had been manifested in the declines during 2008–09. Slowly the fundamentals improved, and then investor mood. Demand, reflected in rising PEs, resulted in improved prices. But it takes plenty of time, which is perhaps why this has been one of the most joyless of bull markets.

Lowell G. Miller founded Miller/Howard Investments in 1984. Lowell has served as President and Secretary of Miller/Howard's Board of Directors, as well as President (Principal Executive Officer and Trustee) of Miller/Howard High Income Equity Fund, and Chairman of the Board of Trustees of Miller/Howard Funds Trust, since the funds’ inceptions in 2014 and 2015, respectively. He began his studies of the securities markets as an undergraduate and has continuously pursued the notion of disciplined investment strategies since 1976. He is the author of three acclaimed books on investing, including The Single Best Investment: Creating Wealth with Dividend Growth (Print Project, 2nd Edition, 2006). He has also written on financial topics for The New York Times Magazine, and has been a featured guest on Louis Rukeyser's Wall $treet Week and Bloomberg TV. Lowell is frequently quoted in financial media such as The Wall Street Journal, Dow Jones Newswires, Bloomberg, Fortune, and Barron's. He holds a BA in Philosophy from Sarah Lawrence College and a Juris Doctor degree from New York University School of Law.