The US Produced More Energy Than Ever

Wednesday, July 23, 2025

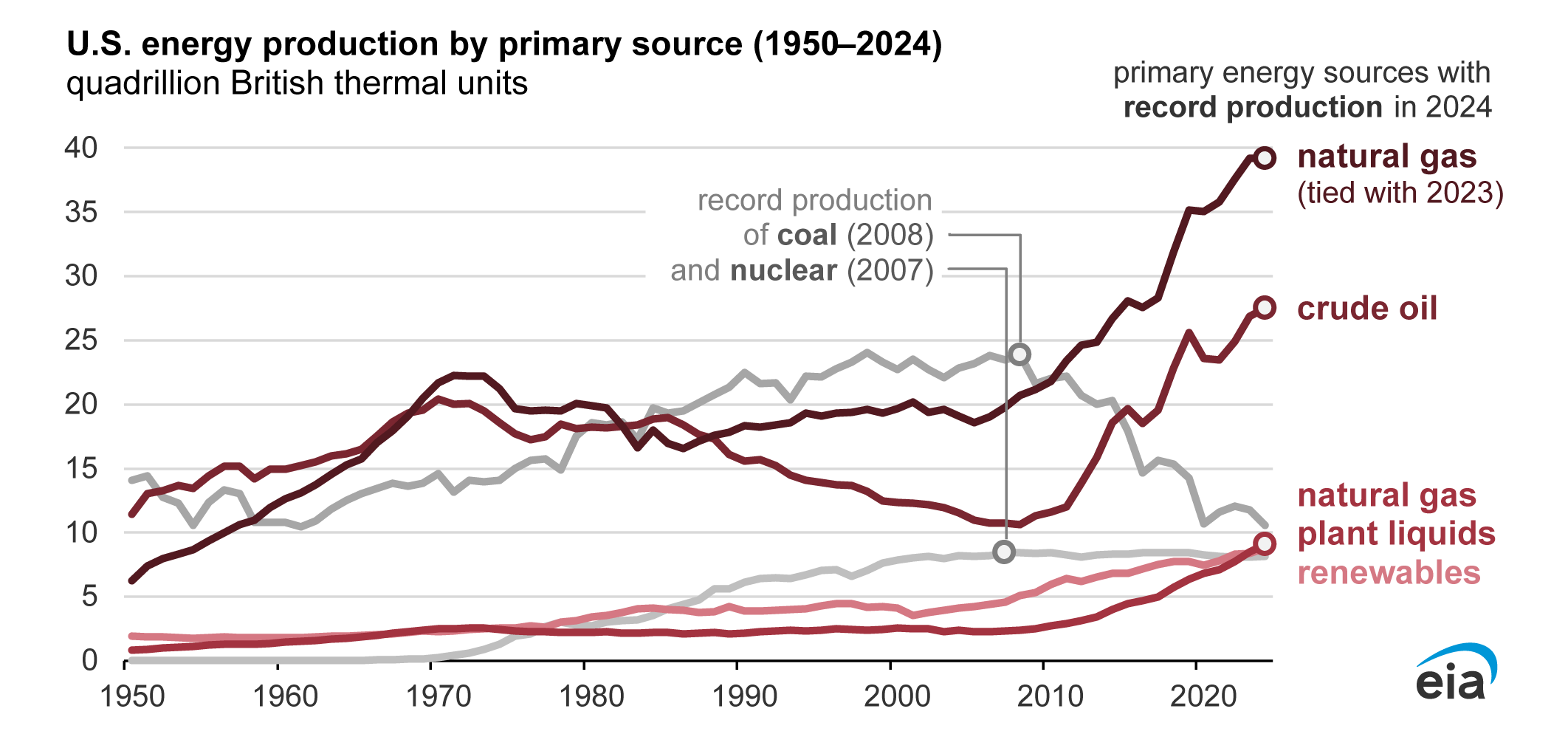

In 2024, the United States produced a record amount of energy, according to the US Energy Information Administration (EIA). US total energy production was more than 103 quadrillion British thermal units in 2024, a 1% increase from the previous record set in 2023. Several energy sources—natural gas, crude oil, natural gas plant liquids, biofuels, solar, and wind—were each at domestic production records last year.

Data source: U.S. Energy Information Administration, Monthly Energy Review

Data values: Primary Energy Production by Source

While we are big believers in expanding total energy production in the US, here is what interests us the most: Natural gas accounted for about 38% of US total energy production in 2024, and it has been the largest source of US domestic energy production in every calendar year since 2011, when it first surpassed coal.

This is a big deal, as many of our midstream energy holdings derive the majority of their income from the production, transportation, processing, and storage of natural gas.

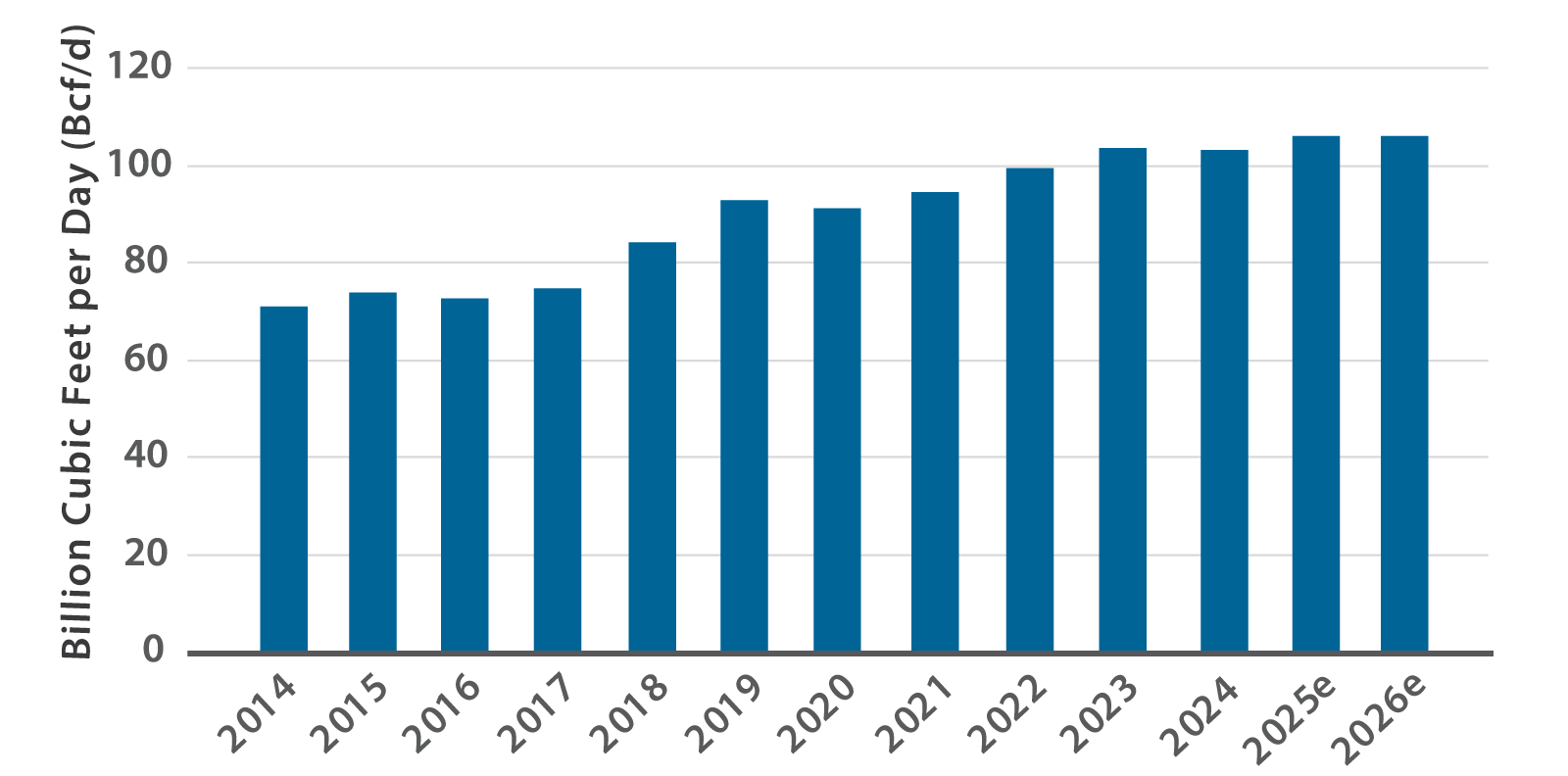

As of July 2, 2025.

Sources: US Energy Information Administration, Short-Term Energy Outlook, July 2025;

Miller/Howard Research & Analysis.

While there have been several headlines recently about the impact of lower crude prices on oil production, we believe there are many tailwinds for increasing natural gas production.

In 2024, the US produced approximately 103 billion cubic feet per day (Bcf/d) of natural gas. But the bigger news is that natural gas production averaged over 107 Bcf/d (an all-time high) in March and April 2025 before falling slightly in May and June 2025. The EIA is forecasting production to average nearly 106 Bcf/d in 2025 and over 105 Bcf/d in 2026.

Why do we expect natural gas production to continue to increase over the next decade? Data centers, liquefied natural gas (LNG) exports, reshoring of US manufacturing, and electrification are the main demand drivers. We believe that these tailwinds will require another ~20 Bcf/d of natural gas (data centers - 6-7 Bcf/d, LNG - 12 Bcf/d, reshoring/electrification - 3 Bcf/d).

We expect that natural gas will be used to meet a large portion of the incremental demand and renewable power sources will supplement as on-demand, dispatchable generation.

Who will be the beneficiaries of these tailwinds?

We see beneficiaries of these tailwinds throughout the energy value chain. We believe that upstream exploration and production (E&P) companies that produce natural gas, midstream energy companies who transport natural gas, and utilities that provide the power to the data centers are positioned to reap most of the benefits.

How is Miller/Howard positioned?

Our North American Energy portfolio is a highly diversified way to gain exposure across the entirety of the North American natural gas value chain, from wellhead production of natural gas to gathering, processing, transportation, distribution, export and related services. Portfolio companies offer exposure to both the volume and price of the commodity. We believe our producers possess decades of low-cost inventories of North American-sourced natural gas and the means to get it to growing electrification, data center, and overseas export markets.

Our MLP & Midstream Energy Income portfolio is 100% midstream, with the majority of the portfolio's income derived from companies that transport and store natural gas. The companies we invest in are volume-driven (versus being highly commodity-price sensitive), and we believe that these thematic tailwinds should have a positive impact on midstream gathering, transportation, and storage volumes—ultimately reinforcing midstream as a source of high and growing income for investors.

Our Infrastructure portfolio is well positioned to take advantage of these opportunities with broad-based exposure across multiple sectors. We expect utilities to benefit from regulated power generation and transmission projects, independent power producers to benefit from tighter power markets (and the resulting higher power prices), and midstream to benefit from higher throughput volumes. Overall, we feel that these growth drivers should bolster the Infrastructure portfolio's ability to provide a high and rising-income stream for investors.

Our Utilities Plus portfolio provides concentrated utility exposure. We expect increasing electricity demand to provide additional opportunities to deploy capital into power generation and transmission projects. Within the regulated business model, we believe this should bolster earnings growth, reinforcing utilities' ability to pay high and rising dividends.

As always, Miller/Howard is dedicated to providing high and rising income to our clients. We expect our portfolios' dividends to be well supported over the next several years as our holdings are poised to participate in these burgeoning tailwinds.

John R. Cusick, CFA, focuses on midstream energy including master limited partnerships (MLPs), utilities, and infrastructure companies. Before joining Miller/Howard in 2013, he was a senior vice president and research analyst at Wunderlich Securities Inc. in New York, covering energy including partnerships focused on natural gas, liquids, and exploration & production. Prior to that, John spent more than a decade at Oppenheimer & Co. beginning his career as a junior analyst on the energy team covering major oil companies, refiners, and exploration and production companies and then as a senior research analyst specializing in the midstream sector. He earned his BA in Finance and Marketing from Temple University, and an MBA in Finance from Fordham University School of Business in New York City.

Adam Fackler, CFA, Chief Investment Officer, oversees Miller/Howard’s portfolio management team and is the designated lead or co-lead portfolio manager on the firm’s products. Prior to being named Chief Investment Officer, he served as Deputy Chief Investment Officer, and he focused on infrastructure companies including utilities, telecommunications, and midstream energy/master limited partnerships (MLPs). Previously, Adam spent 10 years in equity research, including five years at Rodman & Redshaw, KLR Group, and MLV & Co. where he covered exploration & production companies and MLPs. Adam holds a BS in Business Administration with a minor in Economics from Bucknell University.

Michael Roomberg, CFA, focuses on diversified, dividend-paying stocks as well as the energy sector. Before joining Miller/Howard, Michael served as head of water/infrastructure equity research at Ladenburg Thalmann & Co. in New York City. Prior to that he served on Jefferies’ Industrials equity research team. Michael began his career as a research associate at Boenning & Scattergood Inc., a financial services firm in greater Philadelphia, where he specialized in energy exploration & production, and water utilities and industrials. Michael earned his BA in International Relations, Economics, and Finance from University of Wisconsin-Madison. He holds an MBA from the McDonough School of Business, Georgetown University.