Two Views of the Stock Market

Tuesday, June 30, 2020

Society holds conflicting views of the stock market. Millions of people continue to take a long-term view, investing in equities with an eye towards funding retirements that may be decades away. Yet, on a daily basis, commentators use the market as a gauge of how things are going right now. When stock prices are high, politicians and executives are quick to pat themselves on the back and yammer on about how high stock prices are proof positive that all is well. When stocks plunge, the talking heads are just as sure that things have never been worse, with no hope in sight.

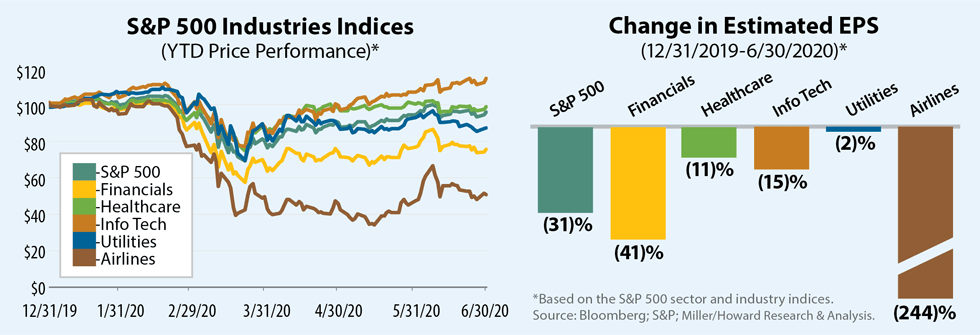

Recent market gyrations have brought this dichotomy into stark relief. The S&P 500 Index peaked on February 19th, then fell by roughly a third over the next five weeks. Since then the market has shot up, rising roughly 40% through quarter end. From the standpoint of a short-term barometer, the market swings are easy to explain. Initially, the market's take on the coronavirus was to ignore evidence that a pandemic had started. Panic set in when it became clear that western democracies would partially shut down their economies to control the spread. Markets roared back when both governments and central banks around the world made it clear that there would be a nearly limitless amount of stimulus applied to the ailing economy. The market recognized that the economy would survive, even as the number of COVID-19 cases and deaths trended higher.

While this year's market swings make sense as a gauge of sentiment, these fluctuations are impossible to understand from the standpoint of long-term investing. The coronavirus presents an enormous healthcare challenge, but in our opinion its economic impact will be finite and relatively short-term. Either a vaccine will be developed, or the disease will run its course through the population. The latter scenario ended the pandemic a hundred years ago. From a human standpoint, that was a tragic outcome, but it did end after a couple of years. We all hope for a successful vaccine, but in any case, the duration of the pandemic will be limited.

By contrast, equities are truly long-duration assets. Stock prices reflect forecasted earnings far into the future. When a stock trades at a price/earnings (P/E) ratio of 20x, the value of next year's earnings is roughly 5% of the total equity's value. So even if earnings are zeroed out for an entire year, the rational drop in market value would be on the order of 5%—not the wild price swings we have seen.

Even sectors with little change in earnings estimates, such as healthcare, tech and utilities, still endured wide swings. Only the downturn in the airlines makes sense given the possibility of major bankruptcies. Otherwise, we can only conclude that the equity market is highly volatile, far more than could possibly be explained by any sort of rational financial analysis.

Implications of Market Volatility

Even to experienced investors, wild market swings can be unnerving, but volatility also creates opportunity. Over the long-term, volatility is what scares many investors away from equities as an asset class. Bond investors clearly sacrifice long-term returns to avoid equity volatility.

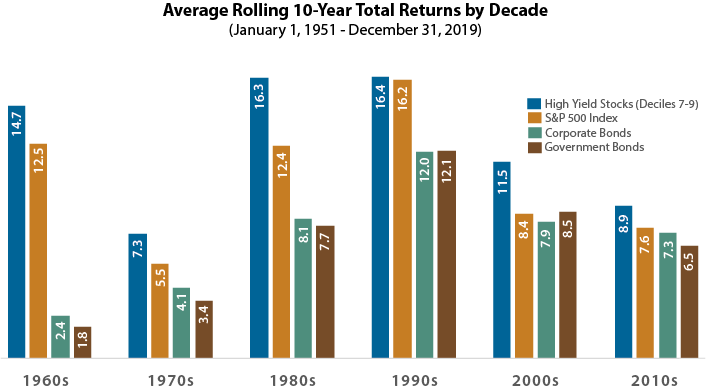

The chart above shows the rolling average returns for high yield stocks, the S&P 500, government bonds and corporate bonds using 10-year holding periods. Equities outperformed bonds in all of these decades, showing the rewards for buy-and-hold equity investing.

What may surprise readers is that high yield equities (Deciles 7-9) outperformed the S&P 500 on average in every one of these decades. Naturally returns can look quite different over shorter periods, as we have seen recently. The outperformance of high-dividend yield stocks over the long-term primarily relates to what a dividend signals about a company and management.

Data are through December 31, 2019. Based on the rolling 10-year annualized total returns, ending each calendar year, averaged by decade.

Source: Miller/Howard Research & Analysis; 2019 Stocks, Bonds, Bills and Inflation ("SBBI Yearbook") and S&P 500 Index data as reported to Morningstar Direct. High Yield Stocks data is provided by Fama/French Research data library (value weighted deciles); Long-term government and corporate bond returns are based on the SBBI Yearbook.

Dividends are a Signal:

- Public companies are run by executives who are strangers to the average investor and should not be trusted blindly. A dividend is a commitment by management to run the firm quarter-after-quarter with shareholder cash return as a priority.

- While management statements should be treated with appropriate skepticism, executives know more about their business than shareholders do. By committing to a regular dividend, management is using more than just words to signal that they expect their business to be resilient, even in a changing environment.

In addition, dividends represent regular cash flow that can be reinvested to compound over time.

In recent years, high-yielding stocks underperformed the broad market. This has largely coincided with the underperformance of value stocks. Dividend investing and value investing are different disciplines, but the universes partially overlap. Many expensive stocks simply cannot afford to pay good dividends. (A company with a P/E of 50x, that pays out half of its earnings, would only yield 1%.)

Value has trailed growth during the last decade primarily for two reasons:

- The run-up of "Winner Take All" growth stocks such as Netflix, Amazon, and Facebook. Investors have rewarded these stocks with fulsome valuations, suggesting that they will maintain high growth rates for decades.

- The increase in bond surrogate stocks, such as some consumer staples and certain utilities, that have reliable dividends but have limited growth potential. Historically low interest rates have enticed some bond investors to buy bond-like equities.

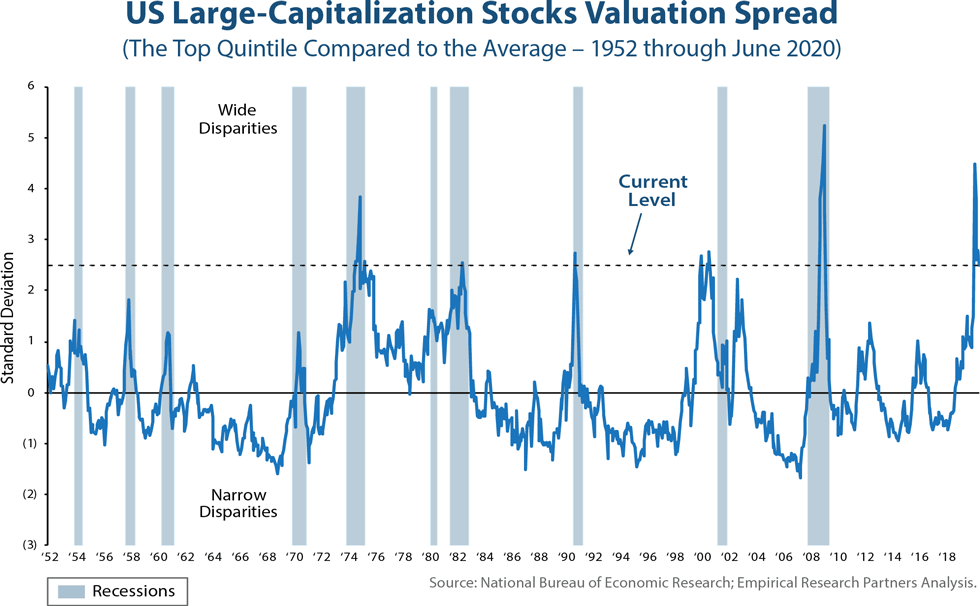

Value investing tends to work best coming out of recessions, following periods in which investors have bid up the prices of stocks offering safety. The relative price of the cheapest 20% of stocks has varied over time, and March 18, 2020 saw a spread so wide it has only been seen two other times in history. Value rallies have typically started during periods of wide valuation spreads. The classic example was the end of the Tech Bubble which led to a sustained rally in value stocks that lasted seven years. Even with valuation spreads narrowing from the recent peak, they are currently just under the level seen at the peak of the Tech Bubble, leaving plenty of room for value to rebound.

In our view, the key catalyst needed for a value rally is for investors to see a clear path to the end to the pandemic. The case count increase in many states is clearly concerning, but we think there will be accommodations to allow the economy to recover. We continue to believe that most jobs can be restructured by social distancing, mask wearing, and temperature checks so that the economy can move forward. A successful vaccine would represent a bright green light, but we would expect the market to trade up strongly on initial news of successful clinical results for any of the hundred plus vaccines under development.

Value rally or not, we expect our dividend strategies to continue to produce reliable income. Over time, dividend income has proven to be an important component of equity returns, and dividends are much less volatile than the overall stock market. A key to dividend investing is avoiding dividend cuts which undermine the premise and the Miller/Howard strategies have largely avoided dividend cuts during this difficult period.

Link to the 2Q20 Quarterly Report ►

Price-Earnings Ratio (P/E)—The ratio of a company's share price to its earnings per share. The ratio is used as a valuation tool and can help determine whether a company is overvalued or undervalued.

EPS—Earnings Per Share