Utilities for Unfixed Income

Monday, September 28, 2020

Utilities offer attractive "unfixed" income—high dividend yields, with prospects for growth.

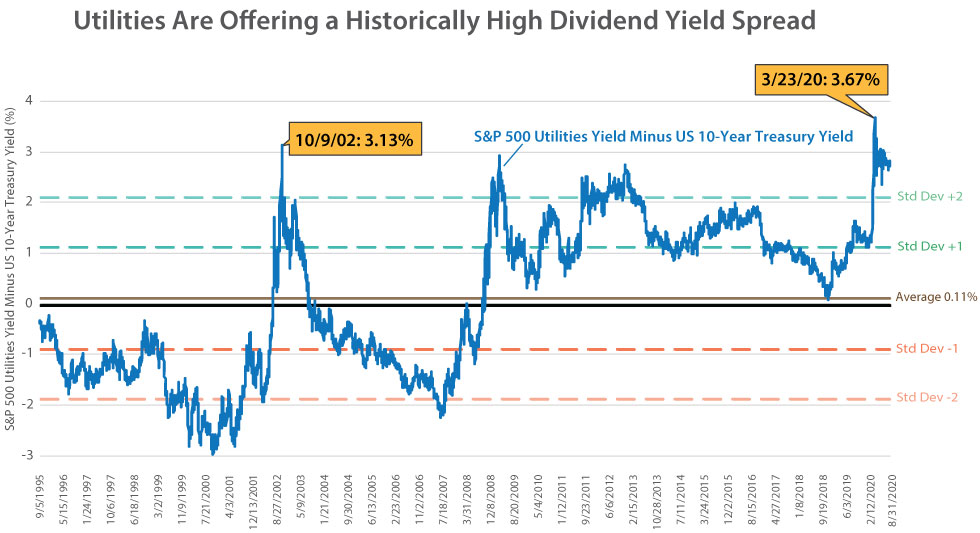

The spread between the utility sector dividend yield versus 10-year Treasury yield remains in the 99th percentile relative to the past 25 years. Why do we view today’s environment as a unique valuation opportunity in utilities?

The spread between the utility sector dividend yield versus 10-year Treasury yield remains in the 99th percentile relative to the past 25 years. Why do we view today’s environment as a unique valuation opportunity in utilities?

With renewed volatility in the markets, it may be a good time to think about an allocation to utilities.

What may come as a surprise to investors is that the traditionally-defensive utilities sector has significantly lagged S&P 500 Index year-to-date*. Utilities have underperformed by over -11% as a handful of mega-cap stocks have driven the broad market higher.

As of August 31, 2020

Source: Bloomberg; S&P; Miller/Howard Research & Analysis

We view today’s environment as a unique valuation opportunity in utilities.

The dividend yield for utilities stocks relative to the US 10-year Treasury yield peaked on March 23, 2020 during the COVID-19 market panic. The spread remains near historic highs, even six months later. Today’s spread between the utility sector dividend yield versus 10-year Treasury yield remains in the 99th percentile relative to the past 25 years.

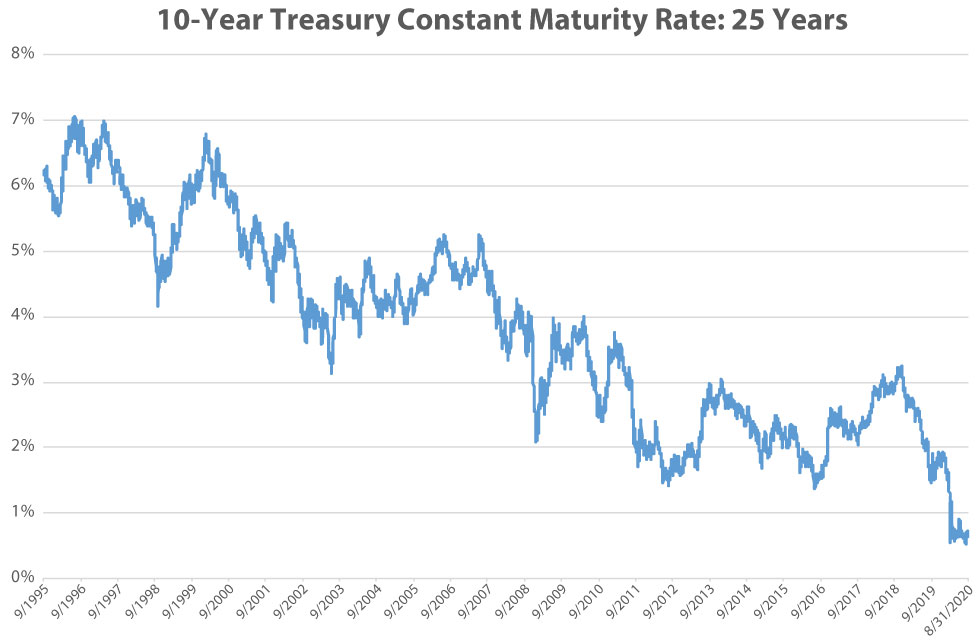

As of August 31, 2020

Source: Federal Reserve Bank of St. Louis

This is largely driven by one half of the equation: the 10-year Treasury is near historic lows. To frame it from an income-perspective, a client with $1 million in savings invested in the 10-year Treasury can expect an annual income of roughly $7,000.** Looking at the Miller/Howard Utilities Plus portfolio, with a current dividend yield of 3.6%, that same $1 million could hypothetically produce an annual income of $36,000 in year one.***

Utilities are, traditionally, a more stable source of income for bond investors who are tired of meager income. With a high current yield—5-times the 10-year Treasury yield—and a strong track record of income growth, utilities can be a powerful alternative to fixed income.***

Sources: Bloomberg, S&P 500 Utilities Index, S&P 500 Index, Federal Reserve Bank of St. Louis, Miller/Howard Research & Analysis

* As of September 21, 2020

** Source: Federal Reserve Bank of St. Louis Economic Research - 10-Year Treasury Constant Maturity Rate (DGS10), as of August 31, 2020

*** Based on the Miller/Howard Utilities Plus portfolio dividend yield as of August 31, 2020

Adam Fackler, CFA, Chief Investment Officer, oversees Miller/Howard’s portfolio management team and is the designated lead or co-lead portfolio manager on the firm’s products. Prior to being named Chief Investment Officer, he served as Deputy Chief Investment Officer, and he focused on infrastructure companies including utilities, telecommunications, and midstream energy/master limited partnerships (MLPs). Previously, Adam spent 10 years in equity research, including five years at Rodman & Redshaw, KLR Group, and MLV & Co. where he covered exploration & production companies and MLPs. Adam holds a BS in Business Administration with a minor in Economics from Bucknell University.