What Are the Tailwinds in Midstream Energy? Natural Gas Dynamics

Tuesday, February 27, 2024

What are the tailwinds in midstream energy? We have written extensively over the last few years about how the midstream sector has changed—better free cash flow and stronger balance sheets. But the question we have been hearing lately is: How can midstream energy’s recent positive momentum continue? Part of the answer lies in the positive ongoing developments with volume growth.

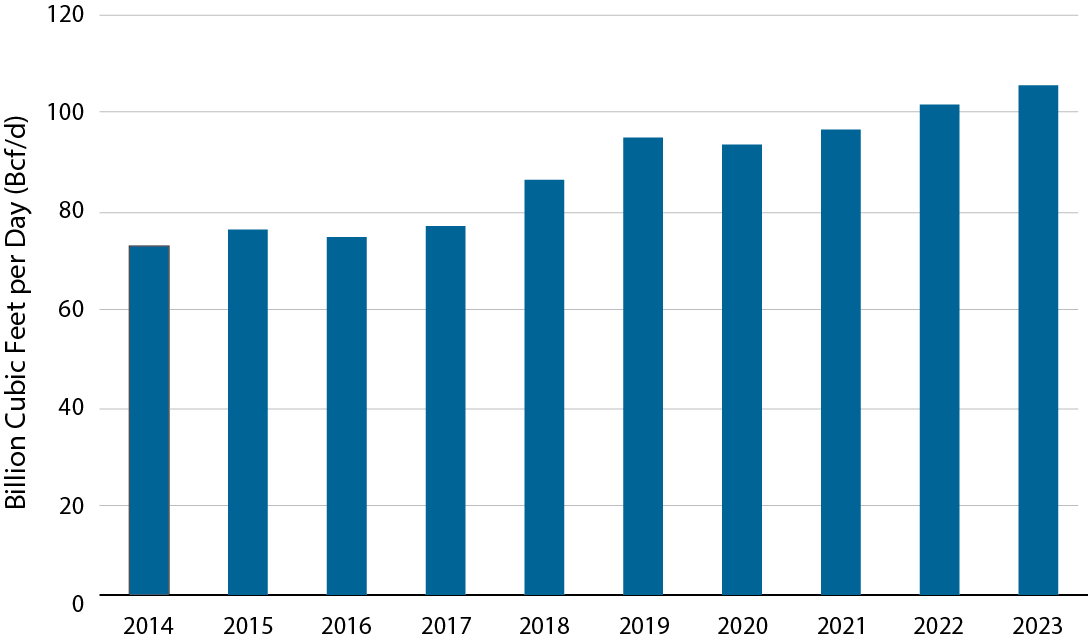

Supply: The US Energy Information Administration (EIA) estimates that US natural gas production averaged a record-high 104 billion cubic feet per day (Bcf/d) in 2023, which is 4% higher than the 2022 annual average. Production averaged 105 Bcf/d in the fourth quarter of 2023, with December recording the highest level for any month on record. Production increased in the Permian Basin (West Texas and New Mexico), the Haynesville Shale (Louisiana and East Texas), and the Appalachia region.

Demand: Overall, natural gas demand increased by 3% in 2023 compared with 2022, according to the EIA. Higher exports and an increase in natural gas consumption for electricity generation helped offset lower residential and commercial sector consumption. Further, the EIA reports that liquefied natural gas (LNG) exports rose 12% in 2023 compared with 2022, and natural gas exports by pipeline increased 9% over the same period.

Sources: Bloomberg; Miller/Howard Research & Analysis.

Why is this important for midstream energy? Increasing production is a tailwind for several of the holdings in our MLP & midstream energy portfolios, as they gather, transport, process, and store natural gas. Of those tailwinds, the biggest may be the increasing liquified natural gas (LNG) capacity in the US. LNG exports have risen from near zero in 2015 to about 12 Bcf/d in 2023 according to the EIA. We believe, between now and 2027, US LNG export capacity will likely double from recently approved and under-construction facilities.

As of February 22, 2024.

Sources: Company reports; Miller/Howard Research & Analysis.

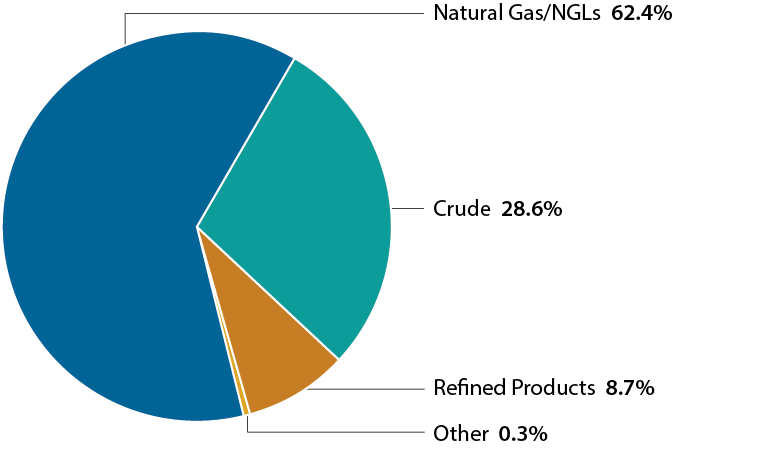

As can be seen in this chart, the majority of the MLP Strategy’s operating income is derived from midstream natural gas operations. [Of course, we would be remiss not to mention that business segments are impacted by more than just a single commodity, most notably natural gas liquids (NGLs) that tend to correlate with oil prices.] Natural gas and, especially, exports offer the midstream sector the opportunity for growth.

We believe the midstream sector provides a unique income solution for investors—and, more specifically, provides income and growth of income.

Importantly, we expect that the higher-quality midstream companies that we invest in will increase their dividends, further enhancing the income provided to investors going forward.

The midstream industry is healthy, in our view. Leverage continues to decline, and shareholders are being rewarded through the combination of higher dividends and share buybacks. In addition, strong free cash flow yields are supportive of current dividends and the potential for dividend increases.

We believe the sector’s stronger balance sheets, vastly improved free cash flow yields, and tailwinds from higher volumes point to a better investment opportunity.

John R. Cusick, CFA, focuses on midstream energy including master limited partnerships (MLPs), utilities, and infrastructure companies. Before joining Miller/Howard in 2013, he was a senior vice president and research analyst at Wunderlich Securities Inc. in New York, covering energy including partnerships focused on natural gas, liquids, and exploration & production. Prior to that, John spent more than a decade at Oppenheimer & Co. beginning his career as a junior analyst on the energy team covering major oil companies, refiners, and exploration and production companies and then as a senior research analyst specializing in the midstream sector. He earned his BA in Finance and Marketing from Temple University, and an MBA in Finance from Fordham University School of Business in New York City.