When 10 Minus 4 Does Not Equal 6

Monday, July 08, 2019

What do people picture when they envision their retirement? Is it living in a tidy beach house where they can spend their days learning how to longboard? Perhaps they could travel the world, only stopping to savour unique cuisines while occasionally dropping in on the grandkids. While dreaming about retirement can be fun, the reality of planning it means considering several scenarios that may be challenging and unexpected. For those who are retired or retiring soon, one of those scenarios involves the real prospect of running out of money.

There are many long-standing financial models applied to retirement planning. One of these is the 4% Rule. Developed by William Bengen in the mid-1990s, the 4% Rule suggests that if you withdraw up to 4% of your nest egg during the first year of retirement, and then adjust future withdrawals according to inflation, your savings should last for at least 30 years. Given the assumption that markets will have an average return of 10% annually, once 4% of the gains are withdrawn, you should still have a 6% annual return for the portfolio’s compound growth. This rule of thumb has been considered a financially “safe” way to plan for retirement.

But when does the 10 minus 4 model not work?

“Market Math”

Consider the Russell, Dow Jones, or S&P indices. Broad market indices are often used to measure the success of a retirement portfolio. And while benchmark numbers can be helpful in showing market results, they don’t reveal the entire story, especially when a retiree is drawing from his or her account and is focused on long-term, financial sustainability. In fact, if investors rely too heavily on the performance numbers of broad market indices, they will always be playing a game of “Market Math” instead of building towards a strong and lasting retirement plan. To see the bigger picture in managing an investor’s portfolio, there are four underlying factors.

The Sequence of Returns

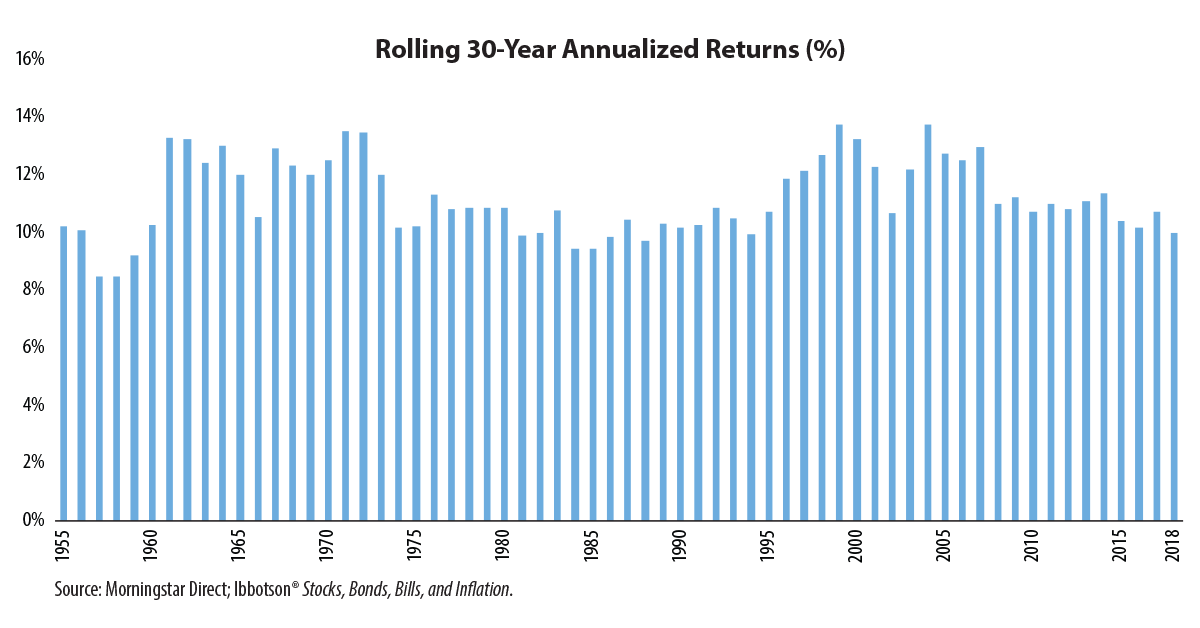

Numbers can be misleading, especially when reviewing the sequence of returns on investments. Using Dr. Roger Ibbotson’s long-term stock market returns, since 1926 the rolling 30-year return of large cap stocks has averaged 11.2%. Yet, there were no instances during those 92 years where the annual return was exactly 11.2%. Instead, there were only six instances during that time period where large cap stocks returned between 10% and 12% in a calendar year.

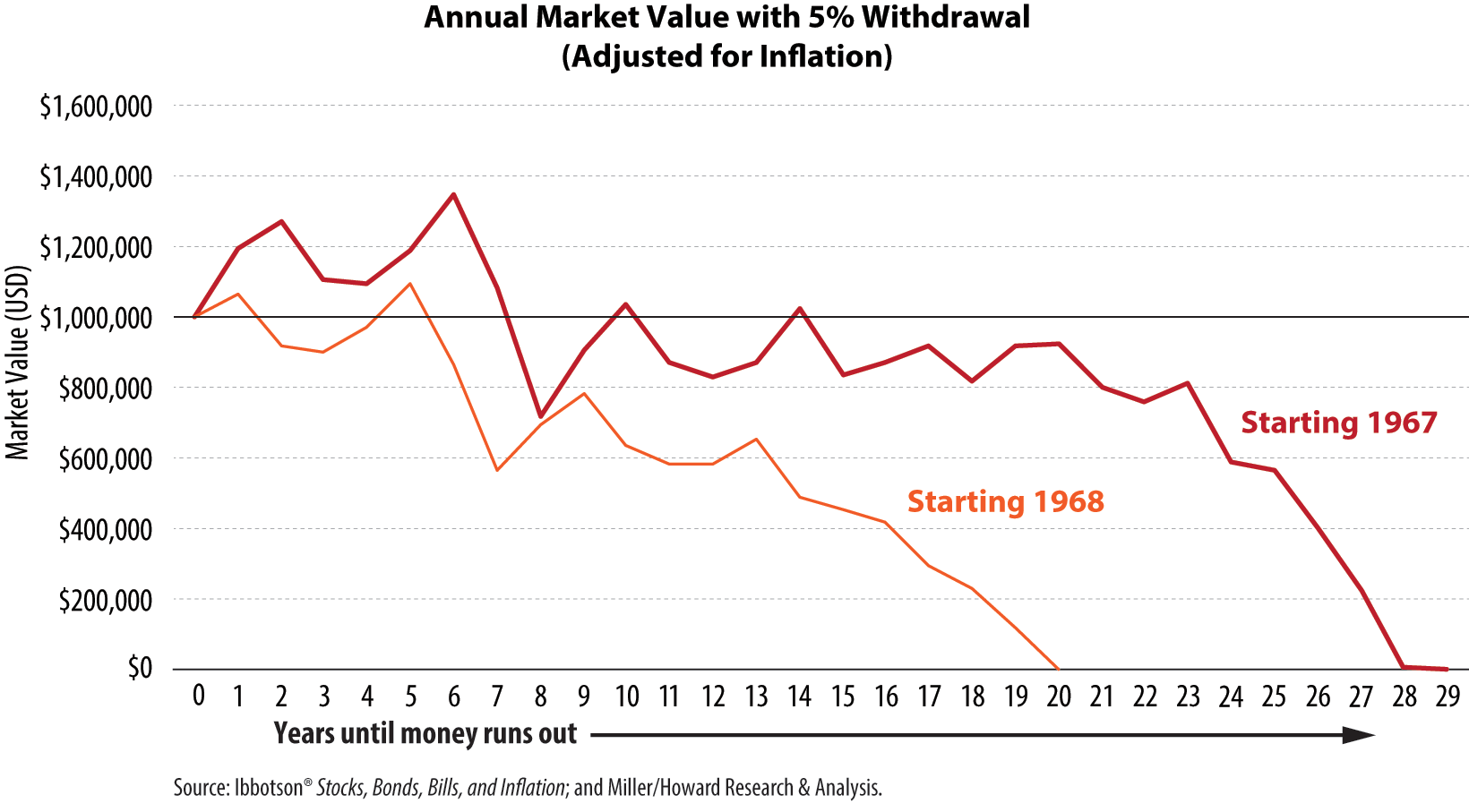

A closer examination of two different points of entry for investors demonstrates why the sequence of returns matters. Per the Ibbotson data, the 30-year period beginning in 1967 saw an annualized total return of 11.9%. This percentage is extremely close to the 12.1% annualized total return for the investor who started just one year later in 1968. Assuming a 5% withdrawal (to account for fees and expenses) adjusted annually for inflation, the individual who retired in 1967 would have run out of money in year 29, while the investor who began in 1968 would have had nothing left in the portfolio in year 20. Why did this one-year difference have such a huge effect? In 1967, there was a greater than 20% return, which the investor from 1968 would have missed. If the long-term goal is to be able to withdraw continuously for retirement income, it becomes essential to evaluate the actual dollar value of the portfolio, rather than focus on just averages and percentages.

Inflation

Increases in the cost of goods and services occur throughout our lifetimes, but its impact is most notable during people’s retirement years. In time, a regular trip to the grocery store results in a bill that is higher. The same items they needed before have become more expensive. There is no guaranteed method to predict the rate of inflation, but the inevitable fact that the cost of living will increase is something to be accounted for in any successful retirement plan. Over the past 10 years, as of the end of 2018, the average annual inflation rate has been 1.8%, but the 10-year annual average during the 1970s was 7.4%. When inflation rises, greater withdrawal amounts are necessary to support a particular lifestyle, which could deplete the value of a portfolio. Withdrawal rates must therefore be adjusted for inflation in order to create a sustainable plan for future spending.

Positive versus Negative Compounding

Positive compounding can have a snowball effect. You have the possibility to earn income on your principal and accumulate more income on top of that income. In a perfect world, the earlier you start saving, the more compounded investment income you earn over time. But due to factors including unfavorable sequence of returns and inflation, negative compounding can actually occur and take a lasting bite out of savings. When combined with an increase in income withdrawals, negative compounding quickly consumes what is left in one’s nest egg.

The (Nearly) Inverted Yield Curve

Fixed-income investments with longer maturity lengths, usually in the form of Treasury securities, typically have higher yields than those with shorter maturities. This results in a normal yield curve where yields slope up as maturity rates rise. When an inverted yield curve occurs, short-term interest rates exceed long-term rates. This type of curve has historically suggested a looming economic recession, though it has not always preceded every recession. Recently, in March of this year, the three-month and 10-year Treasury yields inverted for the first time since 2007, but flipped back approximately a week later. While this is concerning and worth paying attention to, such rapid changes in yield curves only reinforce the need to focus on an investment plan that is sustainable over a long period of time, rather than a plan that responds to short-term market movements.

Does the 4% Rule rely too much on spending from total return? We feel that if the ultimate goal is to ensure a safe retirement, advisors should help their clients understand the differences between spending from total return versus spending from income.

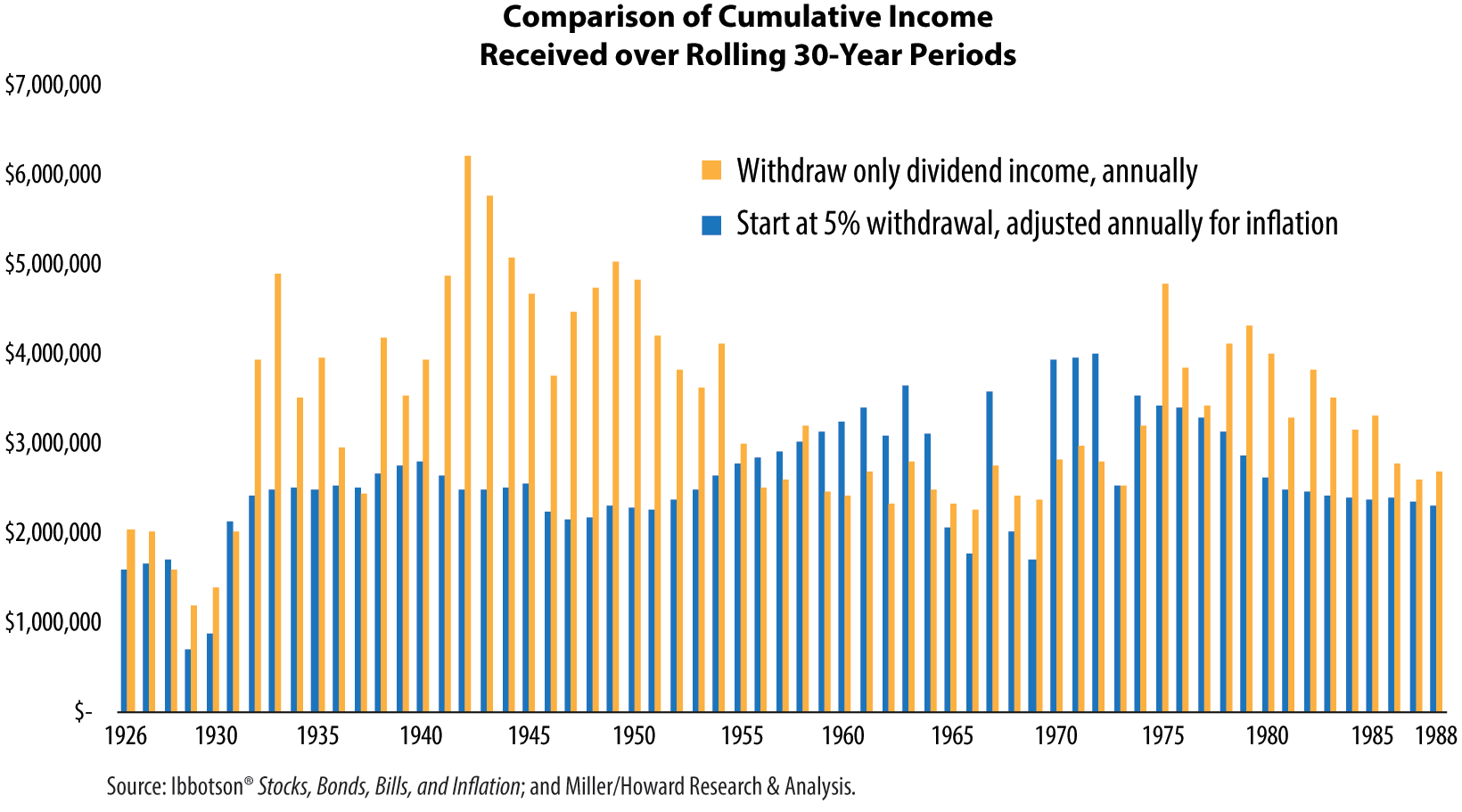

How do you design a sustainable retirement income plan? One method is to adopt an endowment spending model. This involves only using money earned annually for expenses. Instead of withdrawing a fixed percentage each year to accommodate a certain lifestyle, spending from dividend earnings, for example, protects the total retirement fund over time.

The graph above compares the cumulative income received when two different models are adopted. In the first portfolio, a 5% withdrawal, adjusted for inflation, begins from year one until year thirty. In the second portfolio, only dividend income was withdrawn each year. The graph illustrates that the total income received was greater in the second portfolio during 73% of the 30-year periods.

Investing in Higher Yielding Stocks

As a complement to the endowment spending model, it’s worth considering an investment in higher yielding stocks. Dividend and bond yields remain at historic lows, and investing in higher yielding equities can increase the income available for regular withdrawals. As with all investments, there are risks involved in high-yield stocks, so it’s important to consider the company’s characteristics. Here is where the experience of a financial advisor and active management can matter. Understanding the high dividend yield space can help minimize risks when investing in these types of stocks.

The Path to Sustainable Retirement Income

Thinking about potential market shifts and financial setbacks can cause a great amount of anxiety. By using an endowment spending model and choosing the right asset manager to navigate high dividend yield stocks, we believe that equities should remain an integral part of a retiree’s asset allocation.

Analysis does not include transaction costs, taxes, and fees.

Catherine Johnston, CFA, is responsible for oversight of Miller/Howard's sales and marketing departments. She also serves on Miller/Howard's Executive Committee. Prior to her promotion to Chief Marketing Officer, Catherine was a portfolio specialist at the firm, where she acted as liaison between the investment team and the sales and marketing teams. Before joining Miller/Howard in 2016, she worked as a portfolio analyst at AllianceBernstein LP in New York. Catherine received her BA with a double major in Mathematics and Psychology from Hamilton College, Clinton, NY.

Full Bio (PDF)