Which Stocks Offer High Income and Relative Safety? Banks.

Monday, March 04, 2019

Tough regulation has created opportunities that many income-oriented investors have overlooked.

It's been about 10 years since the global financial crisis hit bottom and the Federal Reserve spent trillions of dollars to rescue the US financial system, yet the trauma still shapes many investors' view of bank stocks. Although plenty of US banks now have fortress balance sheets, boast strong earnings, and pay fat dividends, few investors see banks as the safe and attractively priced yield plays they have become, in our opinion.

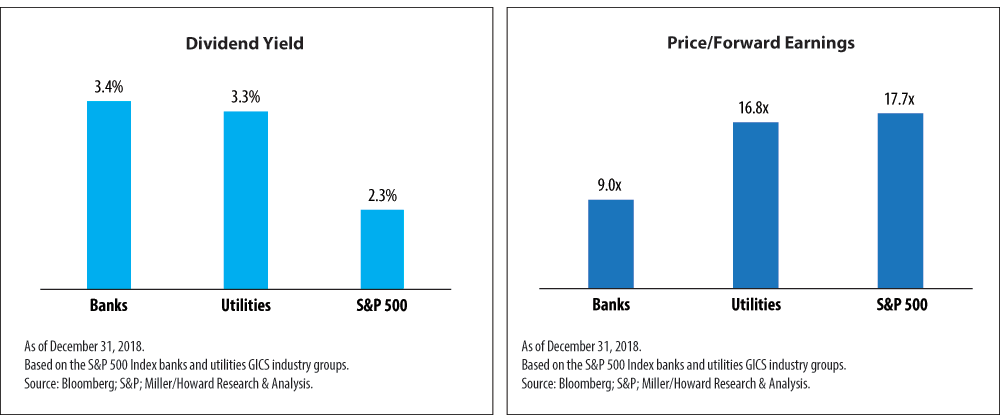

At year-end 2018, US banks were yielding 3.4%, well above the S&P 500's 2.3% dividend yield, and even slightly higher than the yield for utilities, generally investors' favorite traditional yield sector. Yet banks were trading at only 9.0 times earnings, about half the S&P 500's multiple and far below the multiple for utilities, which has expanded dramatically over the past decade as investors sought their safety and yield. Nonetheless, many classic equity income strategies continue to emphasize utilities and avoid banks. The Miller/Howard Income-Equity strategies are positioned differently. Here's why.

Tough Regulation Has Improved the Landscape

In 2008–2009, the Fed didn't just bail out banks and walk away; it boosted capital requirements and forced banks to raise new capital and to retain earnings to meet those requirements. The Fed also barred many banks from engaging in higher-risk activities, such as trading and leveraged lending, while requiring banks that could engage in such activities to maintain even higher capital. As a result, some banks cut back or exited higher-risk business lines that no longer offered attractive returns on capital. Finally, the Fed also required banks to establish better risk-management systems, and the Fed now performs annual stress tests to ensure the banks could survive under difficult conditions.

Meanwhile, the Federal Open Market Committee (FOMC) slashed short-term interest rates to historic lows and purchased bonds, which hurt bank earnings but helped save the US economy. Though plenty of risky loans defaulted, the good loans remained. Ultimately the industry healed, and every US bank that borrowed from the Troubled Asset Relief Program during the crisis repaid its loan.

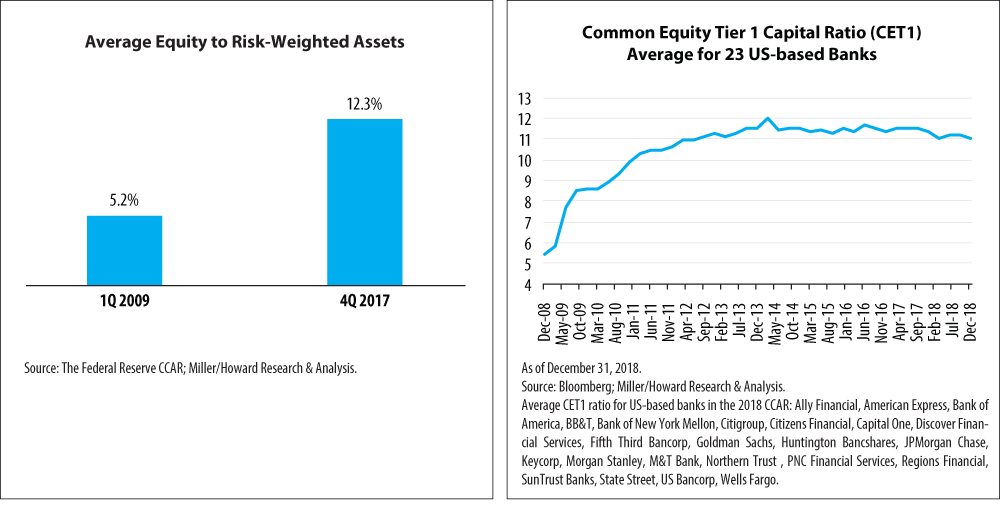

As part of its review, the Fed looks at equity to risk-weighted assets, which can be interpreted as a measure of safety since it reflects the minimum capital that must be held by banks to reduce insolvency risk. Average equity to risk-weighted assets more than doubled from 5.2% in early 2009 to 12.3% at the end of 2017, according to the Fed's June 2018 report on its Comprehensive Capital Analysis and Review (CCAR) of the nation's 35 large banks. In comparison, Lehman Brothers had an equity-to-assets ratio of 3.3%, and Bear Stearns was 3.0% at the end of 2007. Further, in aggregate, the banks tripled their common equity to about $1.2 trillion.

Indeed, banks became so overcapitalized that last June, the Fed allowed many of them to substantially increase dividends and share buybacks. On the same day, all but one of the 23 largest US-based banks* raised their dividends, and collectively, they announced $123 billion in share buybacks. We calculate that the buybacks alone represented about a 6% return to shareholders.

Can It Last?

Some investors worry that the good times won't continue to roll. If the economy slows significantly or contracts, credit losses will rise, taking a bite out of bank earnings. We agree that credit losses will likely rise in time; they certainly can't fall much from today's extremely low levels. But we see the risk over the next few years as limited. Banks don't have many risky loans on their books, and strong job reports suggest the economy continues to chug along. The Fed itself remains bullish on the economy, as reflected by the FOMC's decision to raise interest rates modestly once again in December.

The Fed wrote in its CCAR report last June that it expected bank earnings to continue rising for the next 12 months. That's been true so far, with the US-based banks reporting average pre-tax earnings growth of 8% in 2018, compared to 5% in 2017. (The pre-tax earnings comparison eliminates the one-time surge from the Trump tax cut.) As a result, we expect that when the Fed issues its next CCAR report in June 2019, it will once again allow the large banks to increase cash to shareholders through additional dividends and buybacks.

Not All Are Equally Attractive

Of course, not all banks are the same, and dividend yields and buybacks vary. Some banks have stronger earnings or capital, and some engage in riskier business lines.

Our discipline when selecting stocks for the Miller/Howard Income-Equity strategies looks at dividends, prospects for dividend growth, financial strength, and consistent earnings growth; we also generally prefer stocks at discount to the market. That discipline led to our overweight position in banks.

Within the industry, we generally prefer Main Street to Wall Street banks. Main Street banks make loans to individuals and small businesses and take in customer deposits; Wall Street banks derive more of their earnings and funding from capital markets.

The recovery of the US banking sector has occurred in slow motion over the past 10 years. We think it's time for investors to sit up and take notice.

* US-based banks in the 2018 CCAR: Ally Financial, American Express, Bank of America, BB&T, Bank of New York Mellon, Citigroup, Citizens Financial, Capital One, Discover Financial Services, Fifth Third Bancorp, Goldman Sachs, Huntington Bancshares, JPMorgan Chase, KeyCorp, Morgan Stanley, M&T Bank, Northern Trust, PNC Financial Services, Regions Financial, SunTrust Banks, State Street, US Bancorp, and Wells Fargo.