Why Vaccine News Shifted the Market Toward Value

Friday, January 01, 2021

The news coming out of Pfizer’s vaccine trials on November 9th was truly spectacular and triggered a meaningful shift in the stock market. For months, clients had been asking us, what catalyst could turn the market back towards value and income stocks? Our answer has consistently been that hard evidence of an effective vaccine would jolt the market into, once again, valuing near-term earnings and income.

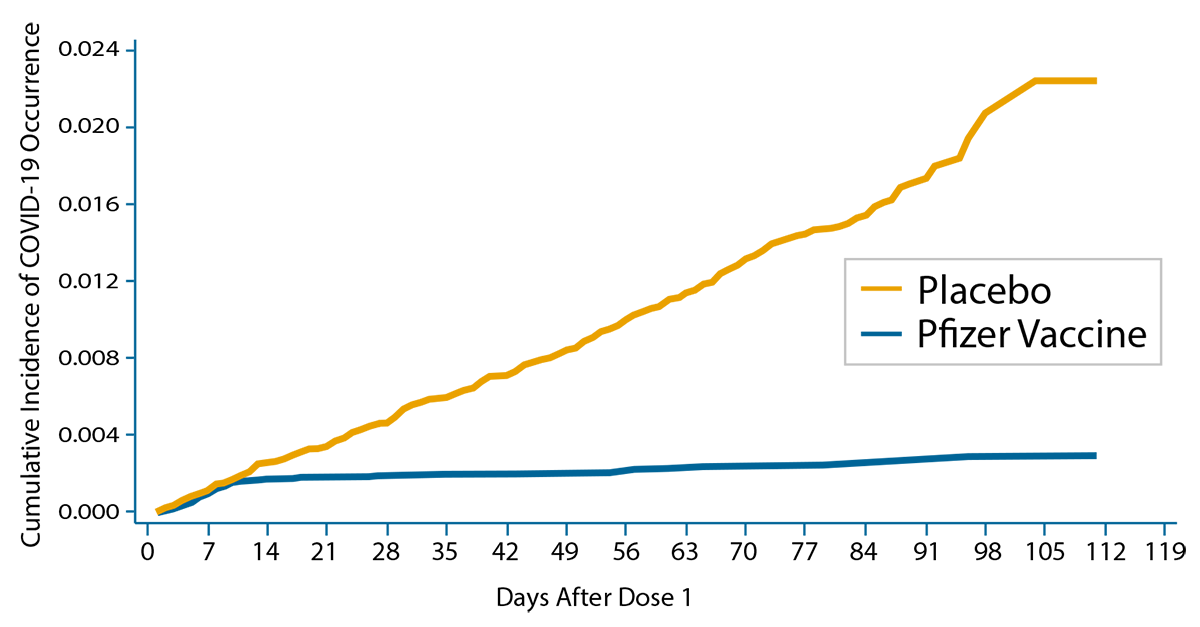

Pfizer Vaccine: Cumulative Incidence Curves for the First COVID-19 Occurrence After Dose 1

* Source: FDA/Pfizer-BioNTech COVID-19 Vaccine VRBPAC Briefing Document,page 58. Pfizer Vaccine: BNT162b2 (30mg). As of November 17, 2020. As of December 31, 2020, Pfizer was held in Miller/Howard’s Income-Equity Strategy; Moderna was not held in any Miller/Howard strategies.

Pfizer’s clinical results were indeed excellent, first described as “over 90%” effective and then shown to be 95% effective when the results were formally presented to the FDA. Pfizer was quickly joined by Moderna with its own vaccine, based on the same messenger-RNA technology, also with roughly 95% effectiveness. In a year of unrelenting bad news, the success of these clinical trials gave the market some visibility into how the pandemic would end.

We view successful trial results for a COVID-19 vaccine as the most likely catalyst to dispel the gloom.

We view successful trial results for a COVID-19 vaccine as the most likely catalyst to dispel the gloom.

In past quarterlies, we have shown how uncertainty created by COVID-19 combined with associated low interest rates pushed the market to favor large-cap growth stocks. Essentially the market looked at the next year and shrugged—why buy stocks based on near-term earnings and dividends when the short-term felt so uncertain? The mega-cap growth stocks seemed to offer earnings growth “forever” without any hard thinking about how the pandemic would be resolved. Investors view earnings far into the future as worth less than earnings now, but extremely low interest rates meant that forecasts of earnings and dividends in the 2030s did not require much discounting. The stampede into mega-cap growth stocks created a headwind for both value stocks and small- and mid-cap stocks. Income stocks were collateral damage, as the expensive mega-cap growth stocks do not pay good dividends, if they pay at all.

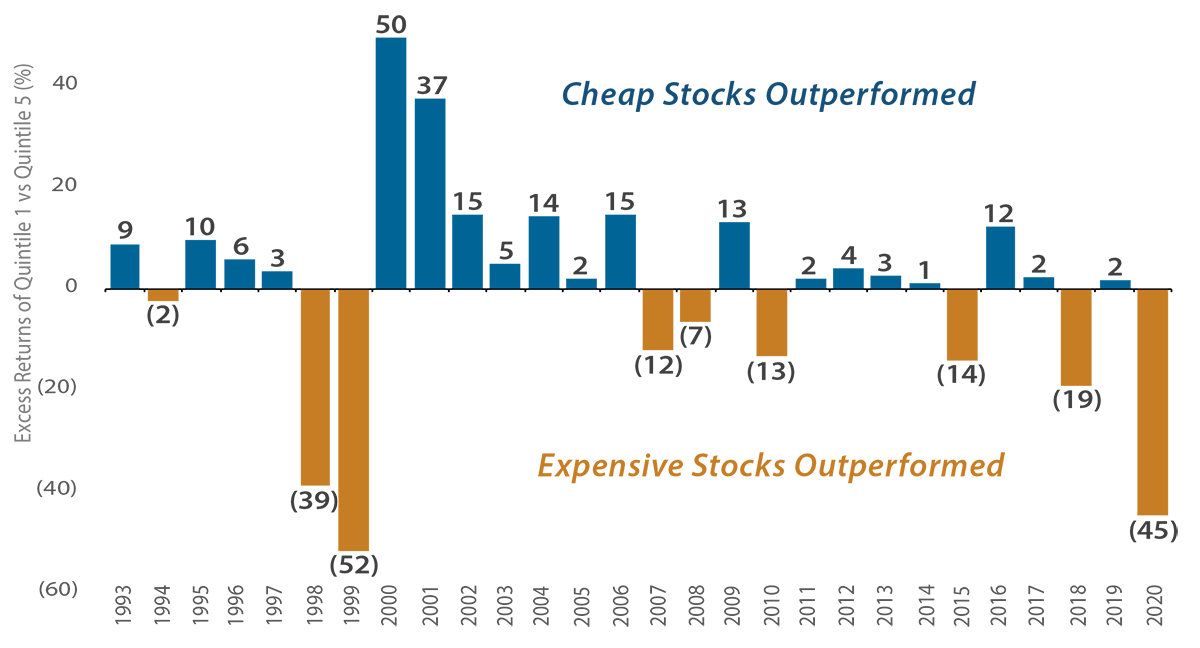

Performance of Expensive Stocks Was Highly Unusual in 2020

S&P 500 Index Forward P/E: Quintile 1 vs Quintile 5

* As of December 31, 2020.

Source: Bloomberg; Miller/Howard Research & Analysis. Quintile 1 is cheapest; Quintile 5 is most expensive.

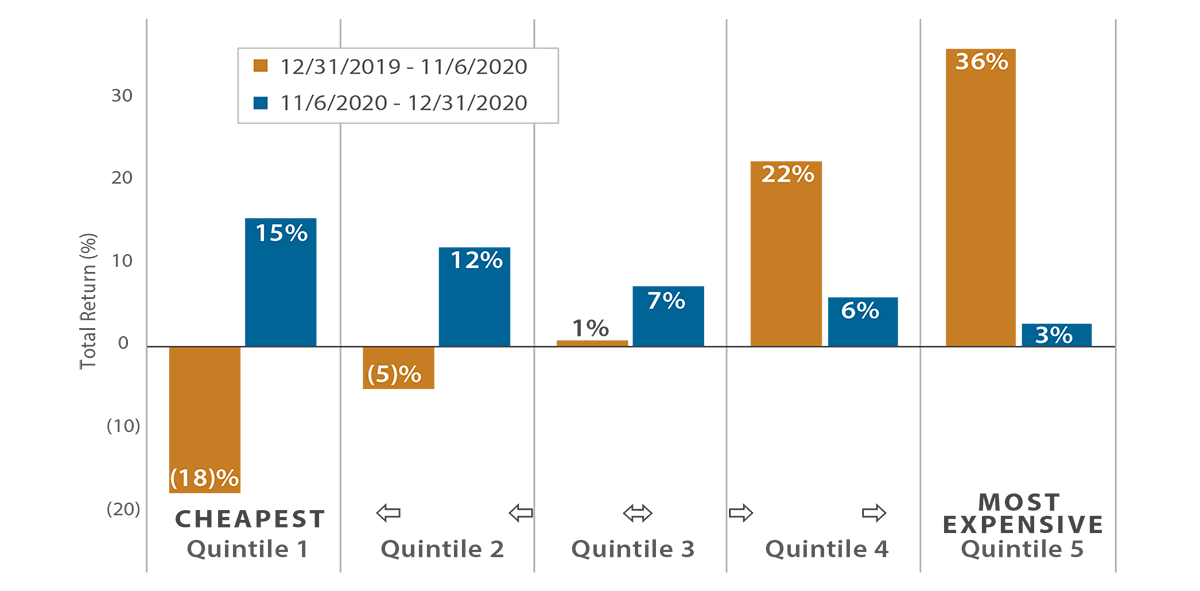

The market turned sharply, beginning the day Pfizer announced the positive news. Let’s first look at the performance of value stocks. The chart above shows the long-term performance of the cheapest quintile versus the most expensive using forward P/Es (price to earnings ratio) as our value metric. In most years, the cheapest quintile of stocks has outperformed the most expensive. For 2020 as a whole, expensive stocks outperformed by a magnitude not seen since 1999. The chart below breaks 2020 into two parts: before and after the vaccine news. Prior to November 9th, the more expensive the quintile, the better the total return. Following the vaccine news, the results reversed in favor of value with cheaper quintiles doing progressively better.

Value Outperformed Growth Post-Vaccine Announcement

S&P Performance Pre- & Post-COVID Vaccine Announcement (S&P 500 Index Forward P/E Quintiles)

* As of December 31, 2020.

Source: Bloomberg; Miller/Howard Research & Analysis.

Will the value rally continue into the new year?

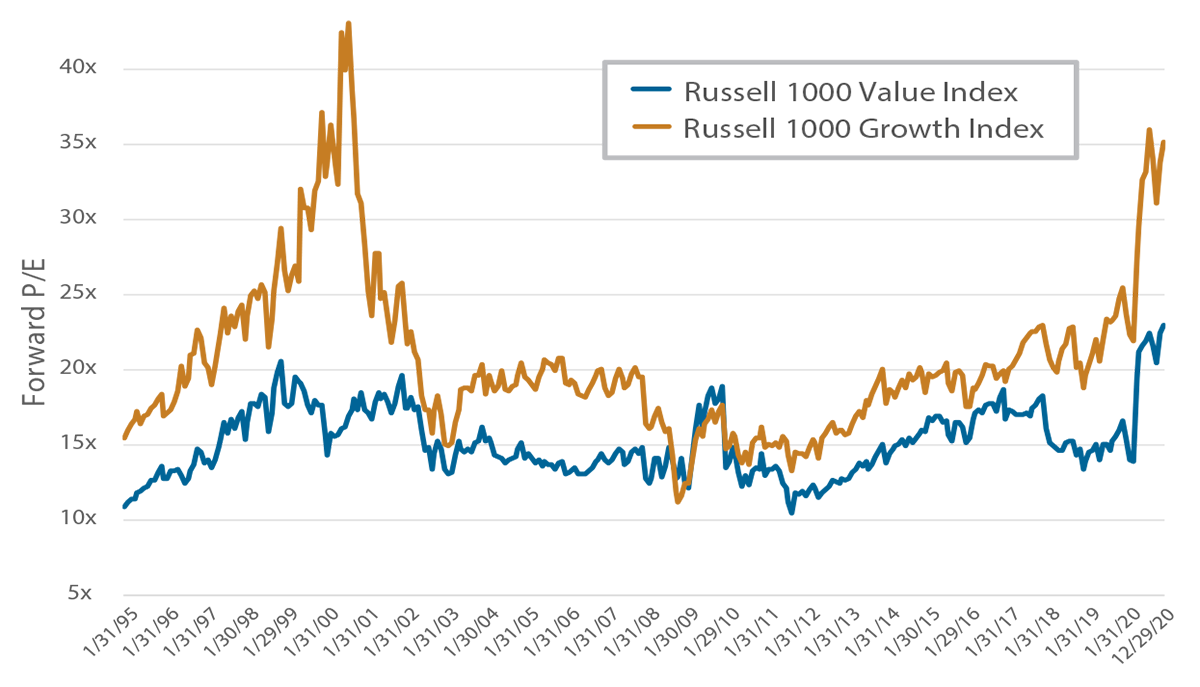

This year has taught us all how difficult it can be to forecast the future, but the set-up remains good, in our opinion. Value rallies typically begin when the spread between expensive and cheap stocks is wide. Comparing forward P/Es for the Russell 1000 Growth Index versus the Russell 1000 Value Index, the spread remains wide despite the market’s recent turn towards value (see chart below).

The Valuation Spread Between Growth and Value Remains Wide

Russell 1000 Value and Growth Indices, Forward Price/Earnings

* As of December 29, 2020. Source: Bloomberg.

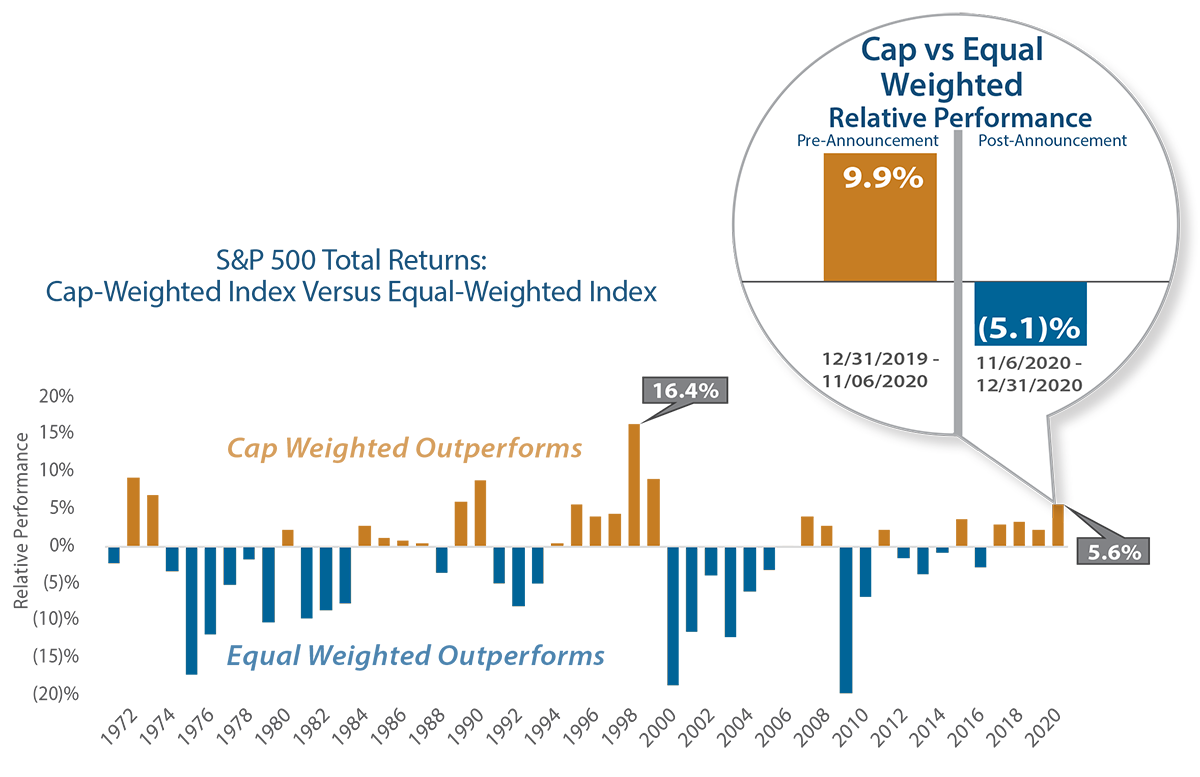

Another trend this year has been the outperformance of large-cap stocks. The Super Six (Microsoft, Apple, Amazon, Google, Facebook, and Netflix) accounted for about 60% of the total return of the S&P 500 Index. Weighting by market capitalization has been important to the returns of the S&P 500 (see chart below). The unweighted version of the index trailed for the year, but this relationship reversed significantly following the release of the vaccine news. As with value stocks, the partial lifting of the fog of uncertainty surrounding the pandemic has prompted more investors to look beyond the mega-cap growth stocks.

Vaccine Announcement Reversed Cap-Weighted Leadership

* As of December 31, 2020.

Source: Morningstar; S&P; Miller/Howard Research & Analysis. Based on the total returns of the S&P 500 Index and the S&P 500 Equal-Weighted Index.

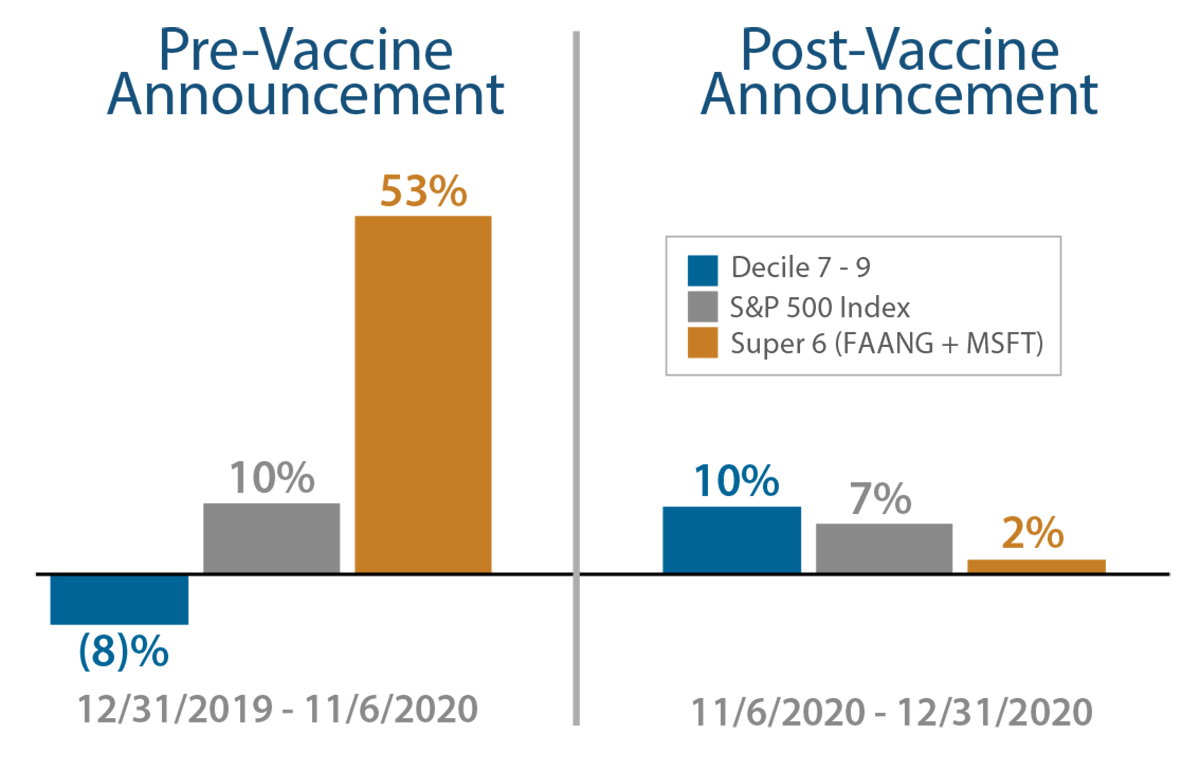

Value, mid/small capitalization, and income investing are three distinct disciplines, but their fates have been intertwined recently given the run-up in mega-cap growth stocks. We’ve seen that value and mid/small capitalization returns improved significantly following Pfizer’s vaccine news, but what about income stocks? We define high-dividend stocks as those with yields in deciles 7-9 when dividend payers are sorted from highest to lowest, with the riskier highest-yielding stocks in decile 10 not included. The chart below, the returns of these high yield stocks versus the S&P 500 and the Super Six, both before and after the announcement of the vaccine results. As you can see, high yield stocks have begun to outperform the broader market while the mega-cap growth stocks have slowed.

High Yield Stocks: 2020 Performance

* As of December 31, 2020.

Source: Bloomberg; Miller/Howard Research & Analysis. High-Dividend Yield Stocks consists of Decile 7, 8, and 9 of a universe of US dividend paying common stocks with a market capitalization or greater than $4 billion. FAANG + MSFT= Facebook, Apple, Amazon, Netflix, Alphabet (Google), and Microsoft.

Looking Forward

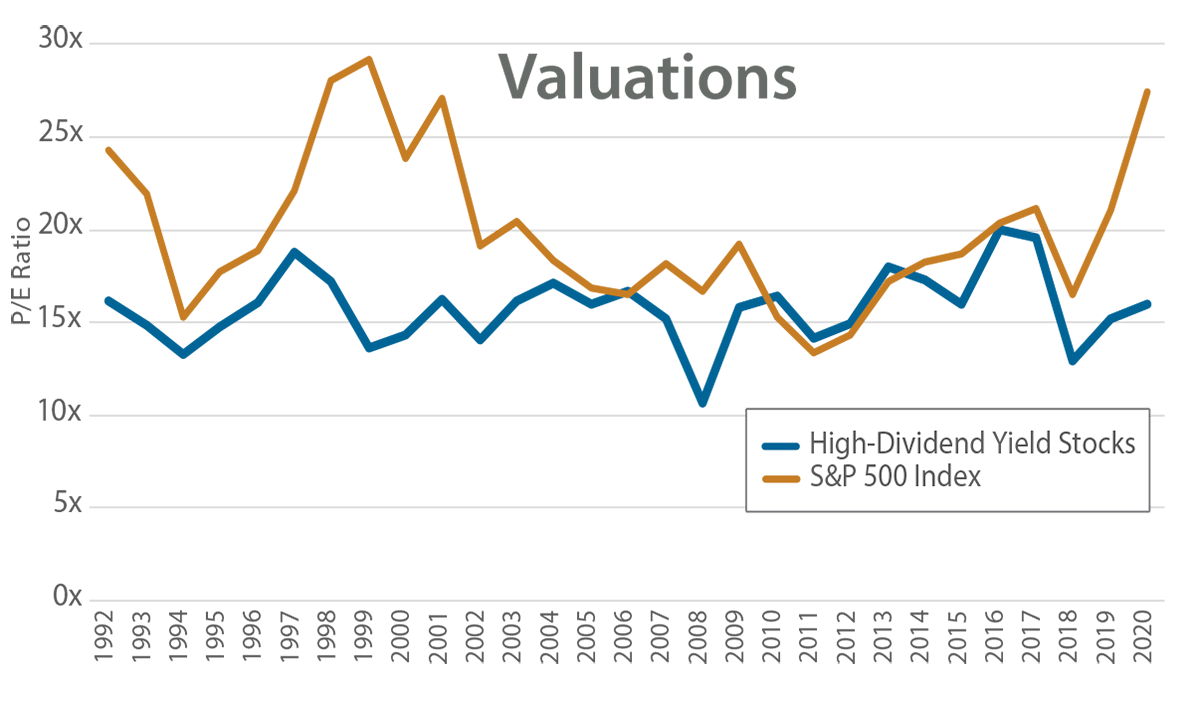

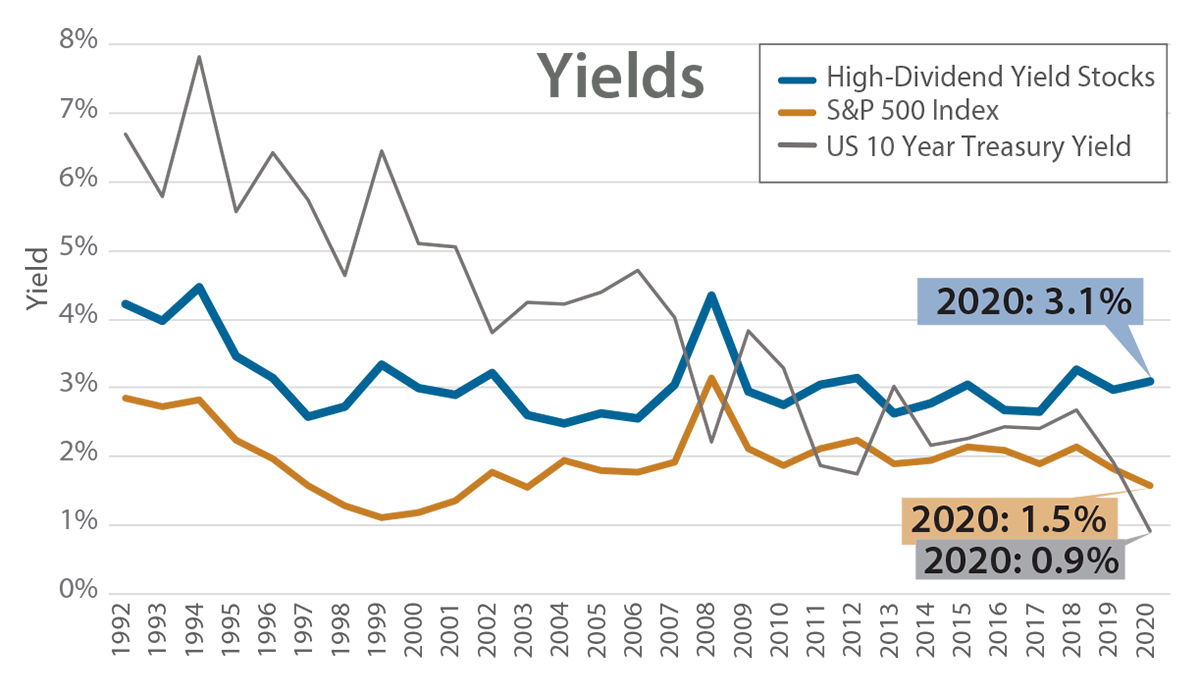

We continue to view this as a good entry point for dividend stocks. The charts below show that dividend stocks remain cheap relative to the broader market and offer superior yields relative to both the S&P 500 and Treasury bonds.

What can go wrong? From a multitude of risks, we’ll focus on three we are monitoring. Regarding the vaccines, there will be production and logistical challenges, but those problems should be resolved given the high stakes. Not so easily set aside is the risk of the virus mutating in such a way that it is no longer prevented by available vaccines. Scientists should be able to respond with an updated vaccine, but time is critical, and we would hate to see this turn into the biological equivalent of “whack a mole.”

High-Dividend Yield Stocks are Trading at a Valuation Discount While Offering a Significant Yield Advantage Relative to History

* As of December 31, 2020.

Source: Bloomberg; Miller/Howard Research & Analysis. High-Dividend Yield Stocks consists of Decile 7, 8, & 9 of a universe of US dividend paying common stocks with a market capitalization equal to or greater than $1 billion.

The vaccine will be supply-constrained early in its rollout, but at some point during 2021, we will learn about the impact of our second major risk: reluctance to take the vaccine. Combining the Pfizer and Moderna clinical trials, the scientific results are based on double-blinded studies including more than 60,000 people. Yet some individuals will have qualms about the vaccine—some may decline while others delay—and this may reduce the number inoculated below the threshold required for a return to normal life.

A significant increase in long-term interest rates is the third major risk we will be monitoring. If all goes well and the economy comes roaring back, long-term interest rates would likely rise. For the reason why, just ask yourself why anyone would tie up their money in a good economy to earn 1%. But higher rates come with their own risks. The high multiples on many growth stocks can only be justified by placing high value on earnings expected more than a decade from now. These far-off earnings will be worth less if rates rise. Conversely, financials should do better given higher interest rates and many cyclicals would benefit from a strong economy. But mega-cap growth stocks form a large chunk of broad indices, so the overall market is vulnerable to higher rates. Just as we saw pundits wonder why the market was up in a terrible 2020 (answer: interest rates), we may very well see pundits asking why the market is falling once the economy truly rebounds.

We continue to see dividend stocks as sound investments. The stocks in our income strategies proved to be reliable dividend payers, even in a difficult year. We seek to invest in companies that have the earnings power to pay dividends now, keeping us away from risky stocks with frothy valuations.

Link to the 4Q20 Quarterly Report ►

Emeritus CIO